Finance options abound as shipping advances towards net-zero

Decarbonising global shipping comes with its share of challenges, including geopolitical and technological risks, and a dynamic regulatory landscape.

An in-depth analysis of the financial health of shipping companies in four key sub-sectors by Standard Chartered’s Capital Structure & Rating Advisory (CSRA) team outlines a pathway for the shipping industry to make real progress over the medium term towards its commitment to achieve net zero by 2050.

The International Maritime Organization (IMO) has prescribed a series of milestones for global shipping’s decarbonisation journey, and the nearest one aims to reduce the industry’s annual greenhouse gas (GHG) emissions by 20-30 per cent, compared to 2008 levels, by 2030.

In pursuit of that goal, the industry, which accounts for almost 3 per cent of global GHG emissions, has undertaken various initiatives, including supporting the development of new vessel designs, clean propulsion methods, and alternative fuels. The IMO has also introduced mandatory decarbonisation measures, such as the Energy Efficiency Existing Ship Index and the Carbon Intensity Indicator.

Additionally, the creation of the Poseidon Principles in 2019 – a global framework for integrating climate considerations into lending decisions that promote the decarbonisation of shipping – is aiding the industry’s transition efforts while penalising laggards. This effort has been a success, with the Poseidon Principles membership boasting 35 signatories, including Standard Chartered, and collectively accounts for about 85 per cent of global shipping finance, according to Chih Chwen Heng, Head of Maritime Research and Decarbonisation, Standard Chartered.

Abhishek Pandey, Standard Chartered’s Global Head of Transportation Finance, adds: “It’s important to have the right mix of incentives to reward companies making progress and deliver disincentives for those that are not decarbonising their fleet. Together these measures can help move the industry forward.”

Navigating headwinds and making headway

The industry’s commitments and efforts to decarbonising a sector as significant as global shipping, comes with its share of challenges, including geopolitical and technological risks, and a dynamic regulatory landscape.

As a recent Standard Chartered CSRA report, entitled ‘Shipping Sector – a sea of change?’ notes, shipping companies face a complex and expensive transition to a decarbonised future, given the sheer number of constantly evolving pathways. However, the report adds, it’s a journey most companies are well-positioned to undertake, at least over the medium term, given the strength of their balance sheets.

Focusing on four key subsectors (Bulkers, Containers, Tankers, and Offshore), the report explores how decarbonisation could impact the balance sheet of shipping companies and how funding gaps can be addressed through various capital structure strategies.

“Fuel consumption globally is still increasing and, despite the move to LNG, we are not yet seeing a decrease in oil use. Oil is now forecast to peak in the mid to late 2030s, versus earlier estimates that it would do so in 2030. The growth in energy demand is happening in parallel with growing demand for LNG,” says Shoaib Yaqub, Global Head, CSRA, Standard Chartered. “That means we need more ships, pipelines, and other key infrastructure, so funding them will probably remain one of the most significant investments required over the medium term.”

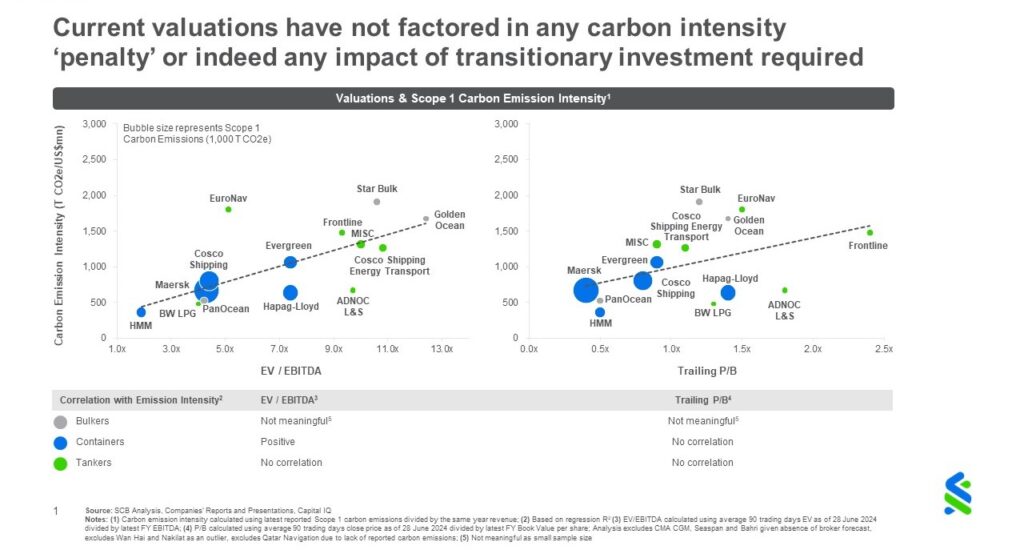

A key message the report conveys is that a change in approach is needed because, while the industry’s transition efforts are expected to burden the balance sheets of ship owners and operators, current valuations also fail to factor in penalties for exceeding carbon intensity benchmarks, or the impact of the investments needed for successful decarbonisation.

This is crucial as upcoming regulatory changes aimed at accelerating the industry’s transition to low-carbon fuels – such as extension of the EU ETS to the maritime sector and the FuelEU Maritime regulation, which will come into effect from January 2025 – will impose additional costs on shipping companies trading into the region. Additionally, the IMO is soon expected to publish guidelines on lifecycle emissions for alternative marine fuels to aid in the standardisation of the fuel pack for decarbonisation, which currently involves different alternative fuel technologies at various stages of readiness and cost levels.

“All of this will impact the balance sheets of shipping companies in two ways: one, by elevating operating expenses as companies foot the premium on alternative fuel costs, and two, by increasing CapEx (capital expenditure) to invest in upgrading fleets and buying new vessels that can run on these alternative fuels. Both will increase funding requirements and necessitate higher indebtedness” says Dieu Anh Khuat, Executive Director, CSRA, Standard Chartered.

Prepared for rough weather: strong balance sheets provide ballast

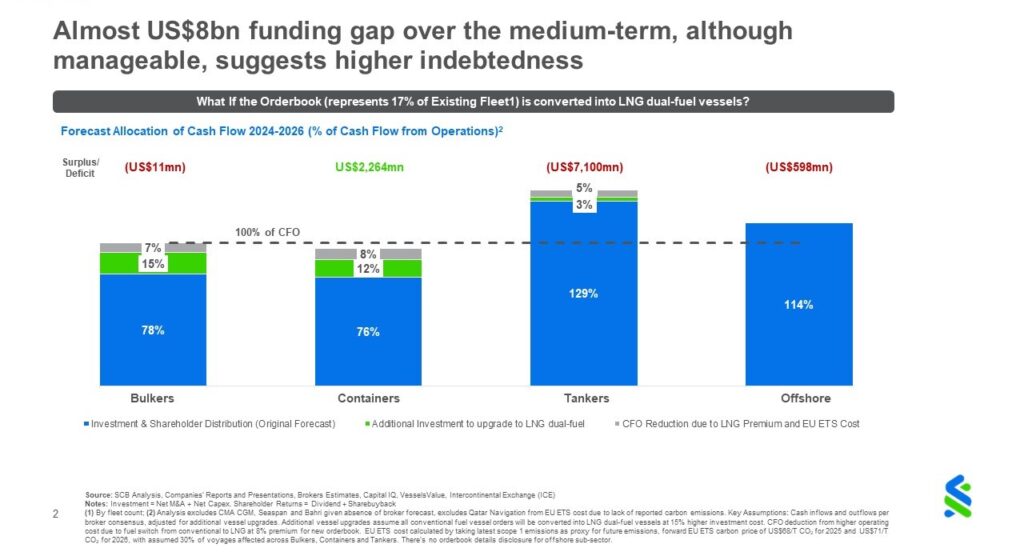

Those investments will need to be sizable given the funding gap, which the report pegs at almost USD8 billion over the 2024-2026 period. Diving deeper into a sectoral analysis, the report studies the potential shortfall in funding over the medium term in the four subsectors.

Assuming that the current orderbook, which represents 17 per cent of the existing fleet is converted into LNG dual-fuel vessels, the report finds that the Tankers subsector is the one with a significant funding gap over the medium term.

Crucially, the potential funding gap could increase over time as the industry needs to invest capital to upgrade ageing fleets to more expensive alternative dual-fuel vessels. For example, LNG dual-fuel vessels could cost about 15 per cent more than conventional hydrocarbon-powered vessels. This finding is especially significant because, as Yaqub notes: “LNG consumption in the world is about to skyrocket and transporting that will require a huge tanker fleet. And this is just one part of the industry.”

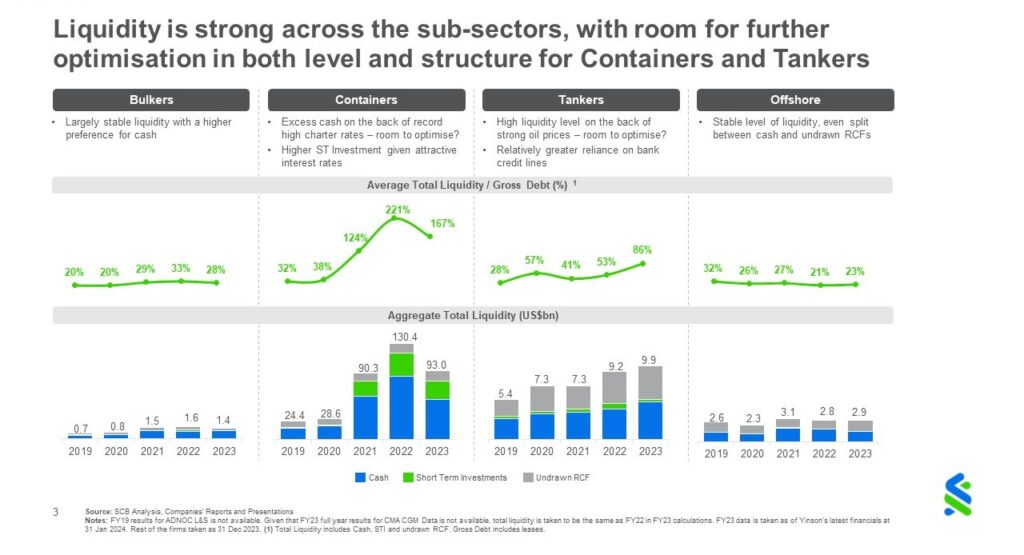

On the positive side, the report’s analysis of liquidity and debt levels of companies in the four subsectors finds that the Tankers subsector is doing well on both these counts, as high oil prices have helped build up a significant cash buffer. It’s a similar story in the Container subsector, where companies benefited from record freight rates in 2021 and 2022, and they continue to enjoy the cash surplus built up over this period.

The report also finds that Container operators took a tactical approach to liquidity management by parking surplus funds in short-term investments to take advantage of high interest rates and enjoy better yields. While Tankers have strategically maintained undrawn revolving credit lines with banks as a liquidity buffer which can be used at a time of need. As a result, both subsectors have ample headroom from the liquidity and leverage perspective. In the Bulkers and Offshore subsectors, meanwhile, liquidity is relatively stable and leverage levels remain comfortable.

The path forward: smart liquidity management, innovative financing to fund the transition

With financial stability allowing shipping companies the flexibility to consider a variety of financing strategies, the CSRA report sets out some recommendations [See Box] to help them properly channel their funds towards the decarbonisation effort.

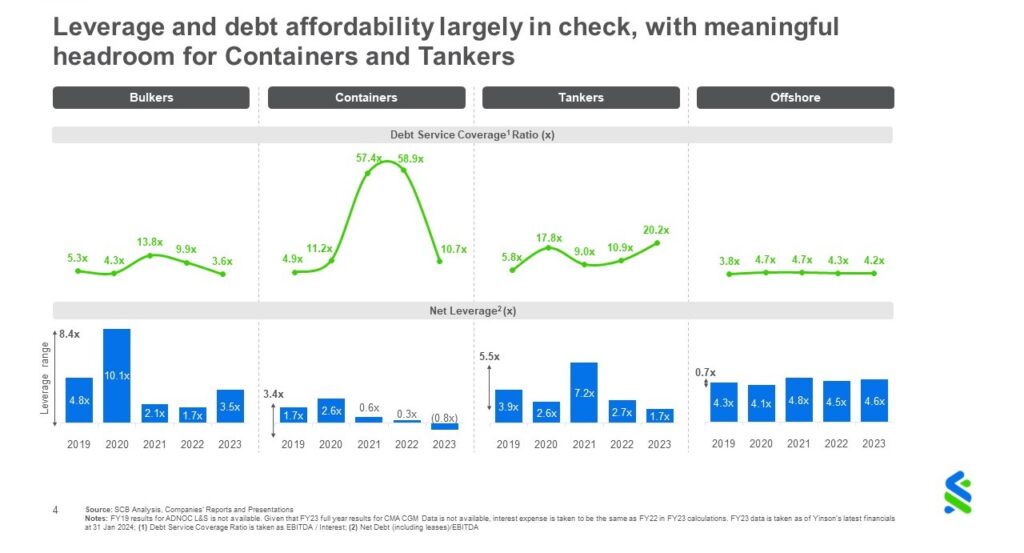

With comfortable liquidity and leverage levels, Tanker subsector companies can afford to utilise the cash buildup towards investments in greening their fleets and take on more debt without impacting their credit profile. Container vessels, which face no medium-term funding gap, can also invest their surplus funds in CapEx and further optimise their healthy liquidity and leverage levels, the report finds.

The Bulkers and Offshore subsectors will need to carefully manage their leverage, which is relatively high. As their ability to service debt is not as robust as those of the other subsectors, the report highlights two key solutions available to them:

The first is to recalibrate capital allocation strategies. Given the high level of discretion in the industry regarding shareholder returns distribution, these outflows can be trimmed, and funds may be prioritised to protect the balance sheet or fund investments. The second lever – one the report found is deployed to some extent by the Offshore subsector – is to diversify into debt-neutral, hybrid capital, which help raise funds while keeping leverage in check.

With the onus resting on the industry to accelerate the transition effort and the scale of the expansion required, the CSRA report urges companies to carefully manage their balance sheets and devise dynamic strategies that capitalise on available funds and leverage capabilities at the right time.

Key Recommendations

- Evaluate investing surplus cash in the transition effort, such as CapEx on upgrading fleets

- Cut back on dividends and share buybacks, and channel those funds to preserve the balance sheet and/or pay for decarbonisation investments

- Diversify to explore innovative structures (including hybrid capital or working capital solution) to limit impact on leverage while raising capital

Standard Chartered as a partner

With a global presence and deep expertise in shipping and transportation finance, Standard Chartered is well-positioned to provide guidance and solutions to companies in the global maritime industry as it transitions towards net-zero.

Some of the critical considerations are: Is the balance sheet ready? Is the capital allocation policy fit for purpose? What should the long-term capital structure be?

Standard Chartered has the unique capability to help companies determine an optimal capital structure that aligns with their strategic objectives while considering the potential impact on their credit positions. The Bank’s services include Advisory, Carbon Accounting, and ESG Reporting and financing.

Get in touch with the team

- Shoaib Yaqub, Global Head, CSRA, Shoaib.Yaqub@sc.com

- Dieu Anh Khuat, Executive Director, CSRA, DieuAnh.Khuat@sc.com

- Annabelle Lin, Associate Director, CSRA, Annabelle.Lin@sc.com

- Abhishek Pandey, Global Head of Transportation Finance, Abhishek.Pandey@sc.com

MiCA a banks blueprint for digital assets success

Regulators craft crypto rules to protect consumers and ensure stability. As adoption grows in Europe, crypto cus…