The way forward for Africa’s financial markets

As Africa’s attractiveness to investors grows, how should it develop its capital markets to further capitalise on this window of opportunity?

Africa’s growth story is coming into its own after a period of tumult. As its attractiveness to investors grows, how should it develop its capital markets to further capitalise on this window of opportunity?

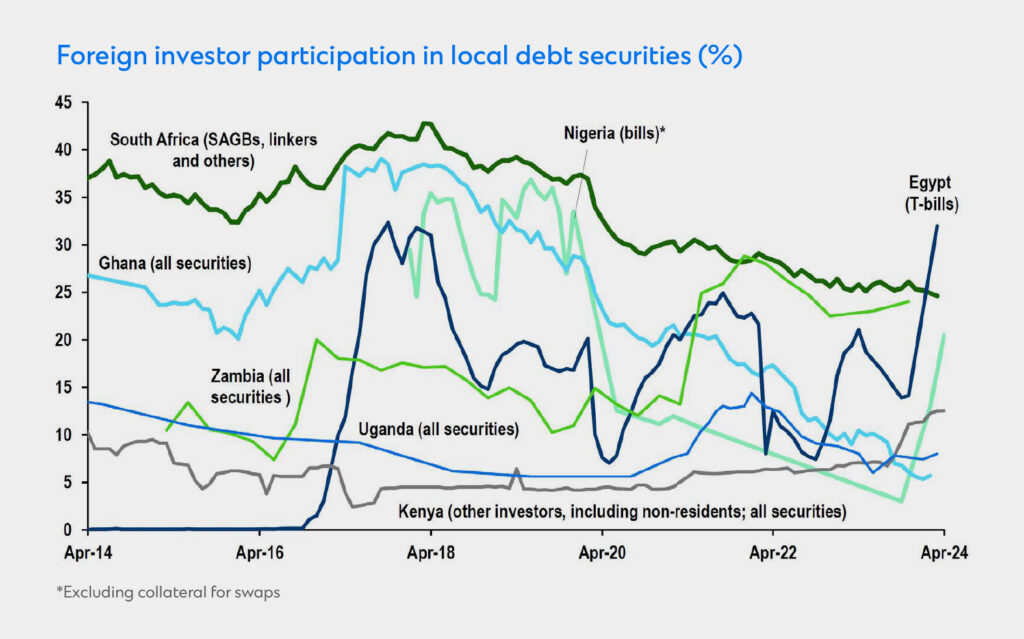

Africa’s major economies are starting to rebound after a period fraught with challenges like grey listings, capital flight pressures, and thin liquidity. As the recovery gains strength across the continent, these markets are becoming increasingly appealing again as investment prospects.

Source: Standard Chartered Research

"There are many green shoots which can start to deliver performance across the markets, and we are starting to see domestic as well as offshore investor appetite returning to the continent"Michelle SwanepoelRegional Head of Financial and Securities Services, Africa, Standard Chartered.

Getting the fundamentals right

For that growth to be sustained, however, Africa’s capital markets will need to advance reforms in three key areas: industry administration and regulation, local market ecosystem reconfiguration, and market deepening.

Market administrative arrangements, that support adherence to the IOSCO principles of securities regulation – which are aimed at protecting investors, keeping markets fair, efficient, and transparent, and reducing systemic risk – is more important than ever in order to establish a robust financial services industry that is welcoming to all participants and trusted. It is crucial for capital markets to address the ambiguities around the responsibilities of fund administrators, managers, and trustees; This is an area where regulatory and administrative arrangements tend to be both incomplete and poorly linked to the actual product, service or operational risks that need to be managed in the provision of services from all stakeholders operating in the execution of robust fund management and performance.

Another priority in getting the fundamentals right is to improve turnaround times for investors– a particular issue for Ghana, Kenya and Nigeria, where trades have a T+3 settlement cycle is to enable investors in these countries to have use of funds and assets as soon after trading as possible aligned to other global markets. Compressing settlement periods would appeal to the countries’ young population, most of whom are aged under 35. Capital markets need to position themselves to address the needs of an emerging generation of investors that is accustomed to online shopping and same-day deliveries and less open to waiting three days to buy an asset and another three days to sell it.

But solutions are at hand, with CSDs across Africa reaching out to counterparts in the US and India for guidance and best practices on moving to a T+1 cycle. Individual markets are also tailoring their approach to suit local characteristics and challenges. For example, in Kenya, the central depository for equities offers investors the flexibility of selecting the settlement cycle at the point of trading. Nigeria’s CSCS is well advanced with the market consultation and regulatory engagement phase of their project to reduce the settlement cycle for equities from T+3 to T+2 with further settlement acceleration planned thereafter. The low levels of connectivity between market infrastructures and investors or their intermediaries is one the most frequently cited impediment to efficient and automated processing which is a key enabler and requirement for settlement cycle reductions. In response, Nigeria’s CSD has set up an interim solution connecting brokers and custodians via APIs to establish faster, straight-through processing that’s less expensive than global communication systems like SWIFT.

Indeed, SWIFT may not be the answer for every market due to cost constraints and relative scale of market activity. Instead, new systems are being developed with the same ISO standards applicable to SWIFT to provide an alternative mechanism for information and data exchange for market participants. Strate, South Africa’s CSD, acquired Trustlink, which operates across the SWIFT network, with a goal to expand it across Africa to offer more affordable messaging services and enhance linkages across the continent.

Fostering a diverse and progressive ecosystem

The continued development of Africa’s Capital market is contingent on the quality of relationships between capital market infrastructures, regulated participants and value-add service providers operating in the data, technology, and retail market segments. The transition from the current state of historic market set-ups to set ups that can support and drive the growth of the industry calls for progressive thinking around delivering a wider range of products while reducing known risks, identifying, and managing emerging risks and developing operational models and regulations that are aligned with these aims. In order to achieve this a diverse set of industry players needs to be optimally configured to deliver products and services that serve an evolving investor base.

Here again, the ecosystem that supports fund and fiduciary services is an example of a system with potential inefficiencies which results in asset managers being burdened with administrative tasks that could potentially be better executed by banks, custodians, depositories, or other players in the ecosystem. Appropriate restructuring of the framework and flexibility to the assignment of regulated responsibilities together with automation, digitisation and leveraging capabilities and technology that already exists for example in the custody environment have the potential to support Asset managers in their focus on portfolio strategies including diversifying their portfolios to maximise returns. This, in turn, would help markets to mature faster and open up further investment opportunities down the line in a safe and well-managed way.

There is evidence that the focus of many countries in the region is on creating the conditions to optimise market structures however, with each country at a different stage of the growth cycle these efforts vary widely in form and objective. In Ghana, the current priority is to restore market confidence, which was impacted by significant debt restructuring as a contingent to IMF funding support in 2023. In response, Ghana’s CSD is moving from a rules-based regulatory system to a principles-based framework. Such flexibility can help authorities focus on outcomes and adapt to an evolving market dealing with unpredictable developments.

Other countries, especially in East Africa, are looking to provide investors with more options by expanding outside their domestic markets. This is being achieved by integrating markets across that part of the continent, which would allow investors to trade in any East African asset from any country in the region rather than just trading domestically. These linkages would then be extended to the rest of Africa once the technology to make this possible becomes available.

Developing a deep and dynamic market

The third factor, market deepening, is crucial for tackling the problem of low liquidity and lack of instrument diversification affecting certain African economies. Digital assets present a significant opportunity to expand available investment choices in Africa over the next five to ten years.

Looking into the future, efforts to deepen capital markets in the region will need to seriously consider the mechanics of introducing tokenised assets into investment portfolios. Beyond this, ensuring that capital raising regimes are enabled to promote the issuance of new and alternative assets that are context specific, that is, accessible and attractive to the continent’s investors will be the starting point. While there is solid potential on these fronts, Swanepoel noted, capitalizing on that will require appropriate regulatory frameworks and a market ecosystem that can support such initiatives.

Ghana’s Securities and Exchange Commission provides a roadmap for establishing guidelines that cover as wide a range of products and issuance types as possible, including green bonds, asset-backed securities, market trading, market making, and even crowdfunding while Kenya’s market infrastructures are exploring opportunities beyond listed companies. Many profitable and well-governed companies may be worth investing in but are hesitant to list. To address this issue, Kenya’s CSD and stock exchange are encouraging more companies to go public while also exploring OTC market possibilities.

Along with expanding options for investors, markets are looking to broaden the investor base. Ghana’s authorities aim to improve financial literacy and make capital market investing more accessible, especially to those who are apprehensive or have had a negative experience due to misinformation. Technology is aiding their efforts to enhance access and investor convenience, as seen in the 2018 IPO of telecom operator MTN. In a historic first, it enabled share purchases using mobile money accounts, with nearly 85 per cent of Ghanaians buying shares from their mobile phones.

African markets will be at their strongest if they continue to work together, and support and leverage each other’s strengths. With ongoing conversations, collaboration and integration efforts, the continent can flourish and increase its appeal to investors both locally and internationally.

As Swanepoel said, “There’s a huge amount of opportunity, and many ways to leverage different market experiences and expertise from an investor perspective.”

This article is based on themes discussed during a panel discussion titled “Africa in the Year 2030 – a forward look into the next 5 years” at Standard Chartered’s annual Frontier Day event in London.

Explore more insights

South-east Asia’s renewable energy future faces hurdles, but…

The rise of innovative funding solutions underscores the region’s commitment to achieving its clean energy goals…