Three reasons digital assets need an independent custodian

As digital assets adoption grows, so too does the need to store these digital assets safely.

The digital asset universe continues to expand – led by Bitcoin – and shows little sign of slowing. At the time of writing, crypto’s market capitalisation was around USD2.3 trillion, down from the all-time high of USD2.76 trillion reached in March, but still around twice the figure of a year ago (Figure 1).

Figure 1: Crypto market cap – 12-month chart

Source: coinmarketcap.com as of May 16, 2024.

Despite Bitcoin’s price drop to around USD 57,000 in early May, recent research from Standard Chartered held that the reversion from the all-time high of around USD 73,000 reached in March 2024 was largely over and, as expected, it has begun to re-trend higher.

In line with Standard Chartered’s research, should market conditions remain conducive for further adoption, Bitcoin remains on target to reach USD 150,000 by the end of the year, while Ethereum, the second-largest coin by market cap, could reach USD 8,000 – up from around USD 3,000 as of mid-May.

In our view, digital assets are here to stay, and institutional interest in the sector, which has grown significantly in the past year or so, will continue to climb.

Evolution of the crypto custody model

This, however, raises the crucial question of custody. Holding crypto is quite different from holding traditional assets like stocks and bonds: If the service provider which stores your crypto (or if your self-custody system) is hacked or mis-managed, those assets could well be lost.

Custody, then, is a fundamental consideration. So, what are the options? Until recently, there were three main, broad types of digital asset custodian:

- Crypto exchanges, whose original purpose was to deliver a trading function – they were not established to deliver custody services, and became custodians by default.

- Crypto custodians, whose core offering was to provide crypto custody.

- Technology service providers like Fireblocks and Metaco, which are not traditional custodians, but whose solutions are used by licenced providers to hold crypto assets.

The issue for institutional clients remains that none of the above-mentioned options are banking institutions and, as is the case today, are not subject to prudential regulation that would require the custody service providers to adhere to the safekeeping of assets under traditional custody rules.

That was not a problem several years ago, when fewer institutional clients viewed crypto as a viable investment; however, with large asset managers and other institutional players now involved, market dynamics and demands are evolving rapidly.

What’s missing?

For years, then, crypto exchanges have operated outside the traditional custody equivalent of a trust. A consequence is that many retail clients would suffer losses when exchanges collapsed, with assets commingled, misappropriated and lost.

In response, some exchanges today have established trusts and have enhanced their regulatory approach – deploying better technology and broader insurance coverage, both of which are positive.

In this way, they remain attractive to some corporate and retail customers. However, large institutions have significantly deeper requirements across risk management, operational systems and controls, balance sheet and regulatory protection.

What institutional clients need

Crypto exchanges have their advantages: They may move faster than a bank custodian; they can add new features and coins at a much faster pace; and they often boast impressive client-facing technology and an enticing user interface.

However, those aren’t the most important factors for institutional clients. The difficulty for institutional clients isn’t accessibility to crypto; it’s that their internal risk management requirements make onboarding crypto exchanges a major challenge. This is because exchanges typically lack three key elements:

- Bank-grade risk management capability.

- The necessary licences.

- Risk capital.

Those are the aspects that our institutional clients want – the additional layers that a regulated bank brings in terms of risk management – with a robust governance risk framework and a resilient balance sheet. It is why Standard Chartered, with traditional custody expertise in our DNA, has moved into the digital asset custody space: Our clients want to know their assets are safe and fully backed by a regulated bank.

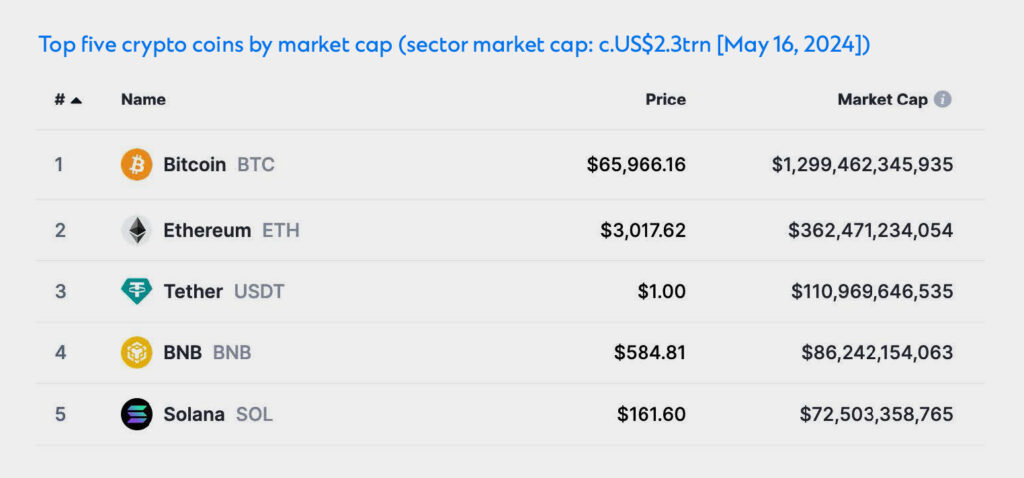

Our custody offering currently extends only to the leading coins like Bitcoin and Ethereum, driven by client demand. With the top five coins alone comprising 80% of the entire crypto market cap (Figure 2), clients are currently not much interested in the rest.

Figure 2: Top five crypto coins by market cap (sector market cap: c.USD2.3 trillion)

Source: coinmarketcap.com as of May 16,2024

Our clients also benefit from best-in-class technology, including cold wallets that enjoy hot-wallet speed via an industry-leading air-gapped solution, and seamless connectivity via the award-winning Straight2Bank NextGen platform and APIs that ensure easy access. Additionally, their entire portfolio, from equities to crypto and beyond, is visible in one place.

Where next?

As mentioned at the start, this industry is moving ahead at a rapid pace, and it’s fair to say it shows no signs of slowing. Beyond the impact of rapid technological change, we expect growing institutional adoption (including the use of stablecoins for online transactions, as Stripe recently announced) and increased regulatory scrutiny – take for example, the EU’s Markets in Crypto-Assets (MiCA) regulation. MiCA comes into effect later this year, and will provide a template for jurisdictions elsewhere.

These shifts and more will drive further improvements in the digital asset custody space, with traditional financial institutions that have the necessary risk capital well placed to offer custody solutions. The introduction of MiCA is set to level the playing field, as it stipulates all crypto-asset service providers in the EU must hold a certain amount of capital.

Perhaps the most significant advance, though, will be the continued penetration of crypto into people’s everyday lives. Visa, for example, is connecting crypto and blockchain networks to its global payment network. The consequence is that growing numbers of institutions and companies will have to hold crypto assets of one sort or another.

As adoption grows, so too does the need to store these digital assets safely. In our view, institutional clients, which must adhere to their own risk and regulatory requirements, will find their optimal custody solution in a bank like ours – a trusted global custodian that is licenced and regulated in multiple jurisdictions, that boasts a strong balance sheet, and that segregates clients’ digital assets in the same way as it does their traditional assets.

Explore more insights

The appeal of infrastructure investment in dynamic markets

Infrastructure investment is a priority sector.