Stablecoins, Blockchains and the Future of Global Commerce

Find out how blockchain can fundamentally reshape how businesses and people transfer value around the world and how stablecoins can transform global commerce.

In partnership with

Authors:

Rene Michau,

Global Head, Digital Assets,

Standard Chartered

Jeremy Fox-Geen,

Chief Financial Officer,

Circle

Key takeaways

- Stablecoins and the blockchains on which they travel can offer unparalleled utility as a new, unified infrastructure for payments, commerce and capital markets built directly into the internet.

- Circle’s USD Coin (USDC) is a blockchain-based dollar that businesses can use to transact across borders, nearly instantly and nearly for free using this “internet of money.” USDC is also programmable, which can enable significant efficiencies for traditional flows along with new ways to use money.

- Standard Chartered sees digital assets as an important and permanent part of the future of financial services and recognizes the potential of stablecoins. Well capitalized global banks have a crucial role in securely managing asset reserves and supporting conversion between currencies in order to unleash the benefits of blockchain for millions of businesses and billions of people.

Sizing up an immense opportunity

Fourteen years on from the 2009 launch of Bitcoin, we are still in the infancy of the blockchain era. While the investment opportunities could be significant[1], there is mounting evidence that payments, ownership of “tokenized” assets and easier dollar access outside of the U.S. can all become near-term use cases that catapult this major fintech breakthrough into the global mainstream. This article will explore the factors that we think could lead millions of businesses and billions of people around the world to start using blockchain for daily commerce over the next few years, potentially resembling the global growth trajectory of the original internet in the 1990s and 2000s.

Blockchain’s significant commercial potential stems largely from its ability to let counterparties settle transactions directly across the fabric of the internet at global scale, almost instantly, at little to no cost, and with unprecedented transparency and auditability. This stands in stark contrast to traditional settlement systems, which rely on one or more intermediaries to transfer funds from one party to another, which comes with costs, delays, opacity and other friction.

In many ways, blockchain is best viewed as a new “internet of money” that can turn any internet connected device into a wallet that’s fully equipped for financial services, which can offer a critical lifeline to people who own a smartphone yet lack access to traditional brick-and-mortar finance. Financial institutions, businesses and individuals can all use this infrastructure without sacrificing stringent global standards around risk and compliance, and while enjoying robust consumer protections.

Stablecoins are the key to unlocking this future. These digital representations of fiat currencies serve as the bridge between today’s banking system and the blockchain based ecosystems, while providing price stability and reducing other risks. The ability for people and businesses to easily transfer value back and forth between the traditional and digital economies is an essential part of blockchain’s value proposition.

As the next sections explore, this means the future success of blockchain is inextricably tied to traditional finance. It is critical for stablecoin issuers to maintain deep connections with strong banks and for those banks to be building digital asset capability.

Banks need to build for tomorrow’s economy

Traditional financial institutions such as banks largely agree that the future of financial services is inextricably linked with the future of digital asset enabled commerce. The vast majority of banks globally are investing in blockchain related technologies, and there is growing demand from all client segments for more efficiency in the financial services ecosystem.

The problems with cryptocurrency in the last few years have revealed that the wider digital assets market will benefit from the presence of regulated institutions. Equally, market participants have articulated the need for a trusted partner in providing related services. As an example, Standard Chartered has launched Zodia Custody and Zodia Markets through its SC Ventures arm and is also investing in digital asset products for institutions within its institutional banking business. It is also working with very selective clients and partners in the digital asset ecosystem to support them with access of banking services and to enable the services which they provide.

With the conviction that digital assets are here to stay, banks have a critical role to play – not just in innovating responsibly to support clients with safe, secure access to both traditional and digital asset products, but also collaborating with regulators, industry partners and fintech firms to shape regulatory frameworks that support interoperability and consistency, and perhaps most importantly, build trust.

Stablecoins are already starting to eat the world

A stablecoin is a digital currency pegged to an underlying reference asset, typically the U.S. dollar. Stablecoin circulation has surpassed $100 billion – much of which is held outside the U.S. In essence, stablecoins equip fiat currency with the internet’s superpowers, so that they can travel like other forms of internet data.

Stablecoins are proliferating globally with a wide range of designs. Yet regulators in different jurisdictions are finding common ground on frameworks to codify reserve quality, transparency standards and redemption guarantees to govern stablecoin issuance (see the regulatory section below for additional context).

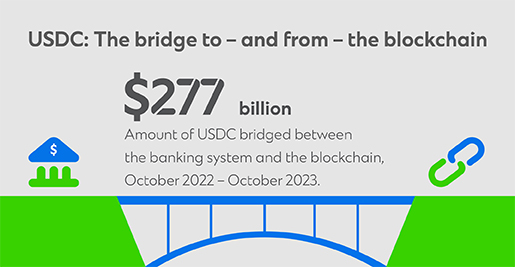

Regardless of jurisdiction, having deep connectivity to the banking system is critical for stablecoin issuers in facilitating broad access and near-instant availability to bridge back and forth between fiat and the blockchain.

Circle is the issuer of USDC, a leading example of a stablecoin that is built and managed under these stringent standards. USDC is a fully reserved digital dollar that is backed 100% by highly liquid cash and cash-equivalent assets and is always redeemable 1:1 for US dollars.

The majority of the USDC reserve is held in the Circle Reserve Fund (USDXX), an SEC-regulated money market fund managed by BlackRock. Daily, independent, third-party reporting on the portfolio is publicly available. The Circle Reserve Fund can contain cash, short-dated US Treasuries and overcollateralized overnight US Treasury repurchase agreements with leading global banks. These are commonly used assets in money market funds because of their daily liquidity and low risk. The remaining portion of the USDC reserve consists of cash, the majority of which is held with global banks, including Standard Chartered, which offers direct access to USDC in Singapore.

In our view, the fact that most stablecoins today are dollar-denominated has actually accelerated their global uptake, given the dollar’s role at the center of global trade. In markets where there are challenges with the value of the domestic currency, there is a higher rate of adoption of USD denominated stablecoins. This aligns with the use of USD in similar markets historically.

We do expect many stablecoins denominated in other currencies to emerge within the next five years. Circle, for example, already offers EURC, a euro-denominated stablecoin issued under the same full-reserve model as USDC.

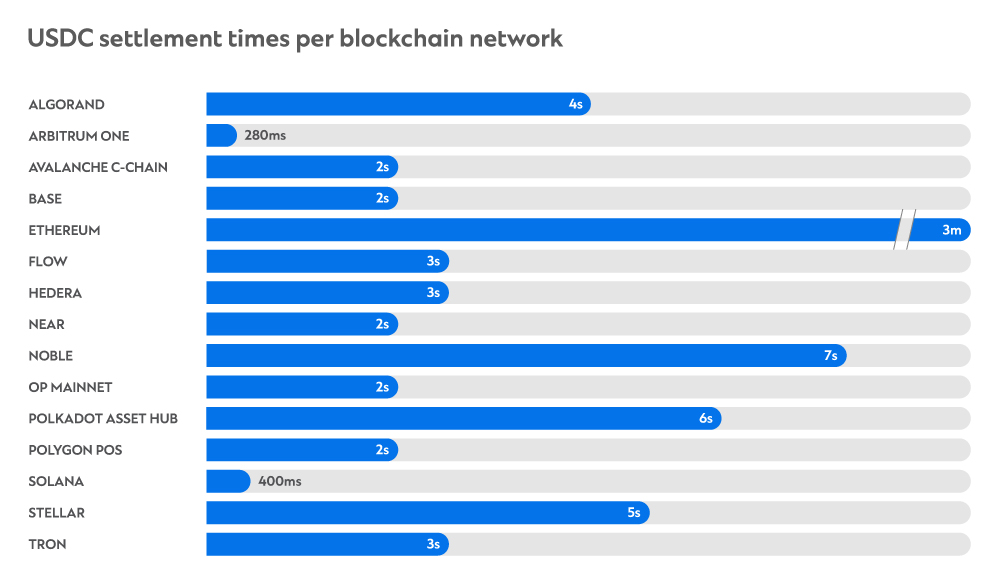

Beyond its inherent attractiveness as an easy way to access the reference currency for global commerce, there are several other factors that make USDC compelling. In addition to the significant speed, scale and cost advantages discussed earlier, USDC is open-source and programmable, which creates tremendous opportunities at a time of rapid evolution in the finance tech stack and the growing ubiquity of APIs.

USDC is essentially a dollar API designed for global commerce. It is easy to program USDC for simple “if/then” conditions, regardless of whether the counterparty is down the street or in a different country.

Here is a deeper look at some key blockchain concepts that make this efficiency and programmability possible.

Why commerce is better on the blockchain

While blockchains are technologically complex, the concept behind them is actually very simple. At their core, blockchains are just digital ledgers that multiple computers maintain simultaneously to keep a shared transaction history over time. Since the ledger is shared and immutable, there is no need for a third-party intermediary to confirm transactions.

Most importantly, it’s not essential for users to master the technical details in order to transact across blockchains, just as card users don’t need to memorize the complex inner workings of clearing and interchange. Additionally, Circle and others are rapidly introducing new services that make blockchain complexity fade into the background.

It’s also critical to note that “blockchain” is not a one-size-fits-all category. Individual blockchain designs can be extremely diverse, and their capabilities are evolving rapidly. As these digital ledgers increase in number and grow more powerful technologically, they are essentially turning into a connected network and forming a brand new financial layer of the internet.

Here are some key ways that blockchain can improve commerce.

- Reduced friction and costs – As noted earlier, blockchains enable faster, cheaper value-transfer compared to legacy settlement systems. This means blockchain offers significant opportunities to improve existing cross-border payments use cases (including corporate and remittance flows), along with traditional capital markets settlement.

- Interoperability – USDC is designed to seamlessly travel across multiple blockchains, which increases its fungibility and ease of use. This interoperability is akin to email, which has coalesced around a single global standard, and unshackles commerce from today’s predominant “walled garden” fintech models. Additionally, since it is programmable, it can connect many financial layers that are siloed today, including fintech, banks and other digital currencies.

Programmability – In 2015, the Ethereum blockchain introduced the first smart contracts. Smart contracts are not contracts in the legal sense, but instead refer to software that is programmed to automatically execute transactions based on pre-set “if/then” conditions. Smart contracts can power tremendous gains in operational efficiency through automation, increase transparency, reduce risks and empower software developers to create a whole new generation of internet-native financial services.

Regulatory clarity spurs greater momentum

Many forward-thinking jurisdictions have recognized the transformative benefits of blockchain infrastructure and are already bringing its best aspects within a strong regulatory perimeter.

Asia Pacific is taking the lead, building on existing mandates to steer toward a cashless society and prominent national, real-time payment systems that process large volumes while running 24/7/365. With regards to stablecoins, the Monetary Authority of Singapore (MAS) already regulates stablecoin issuers through the Major Payments Institutions licensing regime (Circle is fully licensed by MAS as a Major Payments Institution). Hong Kong, Japan and other countries are making progress and are expected to enact stablecoin legislation soon.

Elsewhere, Europe has already passed the Markets in Crypto Assets (MiCA) framework, which sets regulatory requirements for token issuers, crypto-asset service providers (CASPs), stablecoin issuers (ARTs + EMTs) and establishes market conduct rules (e.g. market abuse) for the crypto-asset sector. MiCA is a regulation and therefore directly applicable EU law in every EU country. MiCA licenses are “passportable” into other EU countries.

We are already seeing this increasing regulatory clarity driving more interest in blockchain among traditional businesses.

Near-term opportunities for blockchain

The following are just a few of the uses where we expect greater use of stablecoins and blockchains over the next few years.

- Cross-border payments – The ability to settle dollars globally, almost instantly, and at little cost can help radically reshape a wide range of payments use cases, from global remittances to merchant acquisition/issuance , trade finance and supplier payments.

- Foreign exchange – Stablecoins can help drive significant improvements in FX liquidity, risk and pricing, which can in turn create benefits for both businesses and individuals.

- Traditional capital markets – Many traditional market infrastructure providers, including the Depository Trust & Clearing Corporation (DTCC) and the London Stock Exchange Group (LSEG), are already exploring how blockchain can improve legacy T+2 settlement and introduce new trading opportunities.

- Humanitarian aid disbursement – Ukraine war refugees can receive humanitarian assistance in the form of USDC, which they can store in a digital wallet or cash out locally. In Venezuela, frontline healthcare workers used USDC to pay for medical supplies during the COVID-19 pandemic amid a deepening political and economic crisis.

Talk to us

The rise of blockchain is a major evolution of the internet that can fundamentally reshape how businesses and people transfer value around the world. While it will likely play out over an extended period– much as today’s internet has continued to evolve since email and the first browsers – there are ways businesses can benefit from blockchain right now. Reach out to us anytime to explore how we can help.

[1] “Ethereum’s evolving value proposition.” Standard Chartered. Geoff Kendick. October 11, 2023.

Explore more insights

Trump 2.0 is already changing global behaviour

For President Trump, all is going as planned. Investors need to adjust portfolios to this shift, but avoid over-…