This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Learn the basics of income investing and the four principles you should keep in mind.

What is income investing?

Income investing is when you aim to produce a regular and consistent cash income stream from your investments, either monthly or annually, over a period of time.

This type of investing looks to keep pace with inflation, to maintain purchasing power, in order to achieve a long-term goal, such as income in retirement, or saving for your children’s education.

Understanding an income portfolio

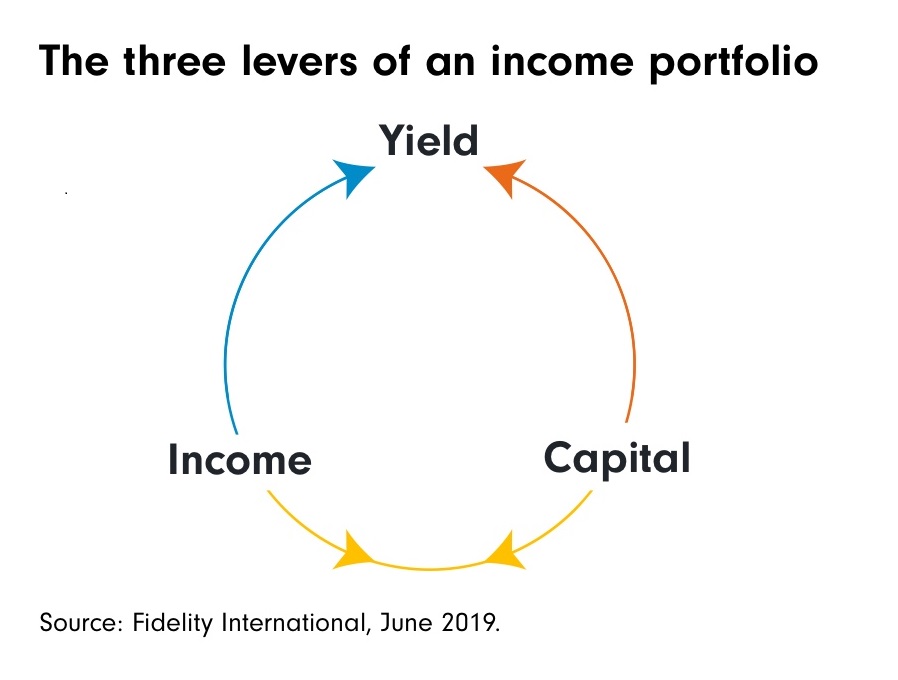

An income portfolio generally contains three levers: income, capital and yield.

While it’s difficult to control all three, an income portfolio prioritises consistent income and capital stability, with yield a function of the two.

A robust income portfolio tends to have investments with good income generating capability and broad capital stability.

Before building an income portfolio, an investor must first decide on the level of risk with which they find acceptable.

Higher income generally means higher risk, but at the expense of reliability, while lower risk sacrifices some income for greater stability.

A good balance can be found by choosing investments that offer attractive income, with some stability.

Four principles of income investing

Here are some things to consider when looking to invest for income:

1. Diversification is key. An income portfolio, like most investment strategies, will benefit from broad diversification across asset classes, geographies and sectors. Having multiple income streams will also help your portfolio to deliver income across different market conditions.

2. Learn about distributions. When choosing an income investment, it’s important to understand the basis for payment distributions. Does the investment have a target distribution and how is it paid? Is this level of distribution sustainable? And will your distributions be paid out of capital if markets go down?

3. Don’t forget fund performance. Regular distributions are not the same as fund performance. Your underlying capital base is the engine that drives income generation and ignoring it could mean you don’t meet your long-term investment goals.

4. Total return matters. Robust Income portfolios will have a good balance between capital stability and income growth. This will help you to maintain and grow your capital base, which also helps to increase the level of real income that you receive.

What you should remember

Income investing is not without risk, and you should always remember:

– The higher the yield, the higher the risk

Higher yielding assets tend to have more risk to compensate investors willing to risk their capital. The same rule applies for income funds, where higher distributing funds tend to take more risk with investors’ capital.

– The impact of inflation

If your income portfolio is not exposed to growth assets, its real value (i.e. after inflation) will fall over time. You can counter this by having a balance between income and growth assets in your portfolio. Income investments like inflation-linked bonds, equities, real estate and infrastructure assets can all help to generate income above inflation.

– Stay focused on performance

And finally, you should always remember, when it comes to income investments, that the yield or distributions offered is not a measure of return. Short-term distributions are only one aspect of performance, especially if they can be paid out of capital, as this could eventually lead to faltering distributions and leave you worse off.

This article is written by Fidelity International.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments, nor does it constitute any prediction of likely future movements in rates or prices or any representation that any such future movements will not exceed those shown in any illustration. This article has not been prepared for any particular person or class of persons and it has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person, and does not constitute and should not be construed as investment advice nor an investment recommendation. Where the article describes any insurance product or service, it also does not constitute an offer, recommendation or solicitation of an offer to buy or sell any insurance product or service, nor is it intended to provide insurance or financial advice. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product is suitable for you.

Standard Chartered Bank (Singapore) Limited (the “Bank”) will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information herein. The Bank makes no representation or warranty of any kind, express, implied or statutory regarding this article or any information contained or referred to in this article. This article is distributed on the express understanding that, whilst the information in it is believed to be reliable, it has not been independently verified by the Bank.

The named contributor to the article (the “Contributor”) does not assume any duty to update any opinions or forward-looking statements, which are based on certain assumptions of future events and information available on the date hereof. There can be no assurance that forward-looking statements, if any, will materialise or the intended objectives or targets can be achieved. Whilst great care has been taken to ensure that the information contained herein is accurate and the data or information supplied by outside sources are reliable, the Contributor does not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information herein. The distribution/dissemination of this article in certain jurisdictions may be restricted by law. The Contributor shall not be held liable as to how and where the Bank chooses to distribute or disseminate the article, in the event that the Bank acts or omits to act in willful default of the Contributor’s written notice to the Bank regarding such distribution or dissemination. Persons into whose possession this article may come are required to inform themselves of and comply with any relevant restrictions. Receipt of this article does not constitute an offer or solicitation by the Contributor in any jurisdiction in which such an offer is not authorised or to any person to whom it is unlawful to make such an offer or solicitation. The Contributor does not purport that it is duly licensed or registered to offer financial services of any kind in such jurisdictions.