This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

An exchange-traded fund (ETF) is a type of investment fund that is listed on a stock exchange (e.g. SGX).

ETFs are passively managed: they aim to track the movement of a particular index (such as the Straits Times Index) and do not try to outperform the index that they intend to replicate. The idea is to match the performance of the broader market.

WHAT KIND OF RETURNS CAN I EXPECT WITH ETF INVESTING?

As ETFs track an index, the return of an ETF matches that of the index tracked less the ETF’s fees.

It should be noted that ETF transactions incur a brokerage fee typically ranging from 0.08% to 0.28% (with minimum commission fees of $8-$28) and SGX trading and clearing fees. Like unit trusts, ETFs also usually charge a trustee or custodian fee of 0.1 to 0.15% per annum on the NAV of the fund and a management fee of under 1% per annum (Source: SGX)

Returns vary depending on the type of ETF invested in and its associated risk profile— for example, an equity ETF is likely to have higher returns than a bond ETF, which has a lower risk profile.

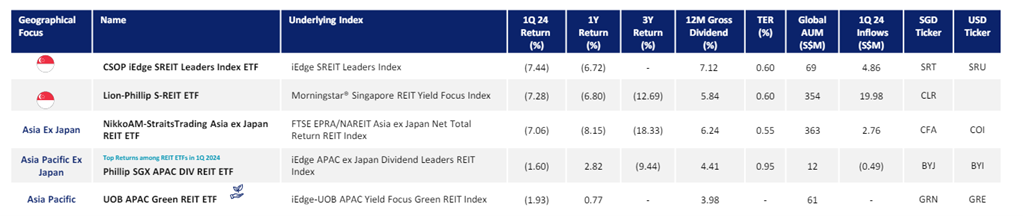

Some ETFs may also pay dividends. For example, the 5 REIT ETFs on the SGX paid out an average dividend of 5.5% with CSOP iEdge SREIT Leaders Index ETF having the highest 12M Gross Yield at 7.12% for the first quarter of 2024.

Source: SGX

EXPLORING DIFFERENT TYPES OF ETFS IN SINGAPORE

The ETFs listed on the SGX can be broadly divided into these categories

Equities

ETFS that track an equity-related index like the Straits Times Index

Bonds

ETFS that track a bond index such as ABF Singapore Bond Index

Commodities

ETFS that track a commodities index

Only one commodities ETF in Singapore which tracks the gold spot price

REITs

ETFS that track various Asian and Singaporean REIT indexes

Only five REIT ETFs currently listed on the SGX

WHAT IS THE STATE OF PLAY OF THE ETF SINGAPORE MARKET?

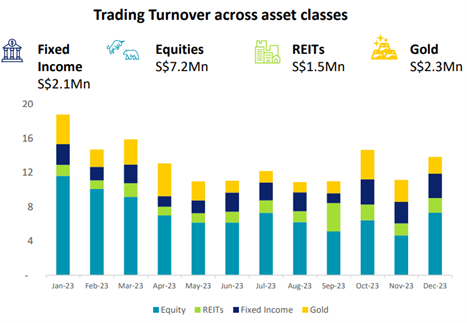

In 2023, daily turnover for SGX-listed ETFs in 2023 crossed S$13 million, according to Singapore stock market data.

The data also showed that for the year 2023, five new ETFs — all equities focused — launched on the SGX and had collectively attracted S$765 million in net inflows.

The information also revealed that as of end-2023, there are 43 ETFs listed on the Singapore stock exchange with combined AUM of a whopping S$10.6 billion.

Source: SGX

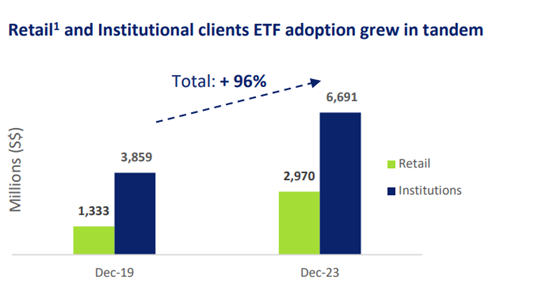

According to SGX Securities data points, retail and institutional clients ETF adoption grew in tandem, rising 96% in the span of 4 years to S$2.97 billion and S$6.69 billion respectively in Dec 2023.

Source: SGX

WHAT ARE THE MAIN ADVANTAGES OF ETF INVESTING?

Low Fees

ETFs’ fees can be much lower compared to actively managed unit trusts.

Without the need for active fund managers and related researchers for stock selection, cost savings can be passed on to investors.

Instant and Convenient Diversification

Investing in an ETF can be equivalent to investing in an entire basket of securities, thus providing instant diversification.

Investors will not have to make multiple investments to achieve diversification.

Less Time

Since ETFs are part of a passive investment strategy, less research and due diligence may be required compared to actively picking out securities.

Less time is needed to monitor performance since ETFs are typically held on a long-term horizon

WHAT ARE THE MAIN DISADVANTAGES ASSOCIATED WITH ETF INVESTING?

Potentially Higher Costs

Although ETFs generally have lower fees compared to actively managed funds, they may still have higher costs than buying individual stocks/ bonds due to management fees.

Potentially Missing Out on Growth Opportunities

ETFS do not cover the entire range of the market.

Investors may miss out on growth opportunities from smaller stocks that are less represented on indices.

Since ETFs only aim to match market performance and not beat the market, potential returns are limited to the performance of the underlying index.

Lower Dividend Cashflow

Investing in equity ETFs is likely to yield lesser dividends compared to when investing in dividend stocks.

Lack of Control

Less control over your investments. For example, if an ETF follows several particular securities that comprise an index and they suddenly fall in price, investors cannot reduce their exposure to only those securities.

WHAT ARE THE MAIN RISKS INVOLVED WITH ETF INVESTING?

Market Risk

Investing in ETFs is investing in the broader market, meaning your investment is still subject to market risk.

Liquidity Risk

ETF markets may become illiquid in times of high volatility, particularly ETFs tracking less-liquid indexes. The result could be a distortion in the prices of the ETF shares.

Tracking Risk

ETF performance may not match the performance of the underlying index perfectly.

While an ETF attempts to perfectly mimic the performance of the underlying index, there is usually some degree of tracking error.

THE KEYS TO CHOOSING AN ETF FOR YOUR PORTFOLIO

If you’ve already determined that you want to have some passive investments in your portfolio, then ETFs can be a good option.

Here are a few key tips when choosing an ETF to invest in.

Key #1: Know which asset class you want to invest in

Understand which asset class (ie equities, bonds, REITs, gold) matches your risk profile best.

For example, invest in an equity ETF for greater potential returns but at a higher risk or invest in a bond ETF for lower returns but at a lower risk.

Key #2: Aim for the lowest fees and expense ratios

Even a small difference in fees can make a big difference over the long-term.

Since most ETFs are competitive on share price, choose the one with the lowest costs.

Key #3: Pay attention to tracking error

Tracking error indicates how closely an ETF is tracking the underlying index.

Tracking error figures should be published on an ETF’s fact sheet or prospectus.

Key #4: Look at liquidity

To mitigate liquidity risk, look at an ETF’s trading volumes which are publicly available on the stock exchange’s website.

ETFs have helped bring investing to a whole new generation.

For those who shy away from stock picking and actively choosing securities, ETFs can allow them to invest in the broader markets at lower costs. Investing in ETFs is a growing worldwide investing phenomenon.

AT A GLANCE: ETFs, STOCKS + UNIT TRUSTS COMPARISON

ETFs

Stock

Unit Trust

Diversification

Yes

No

Yes

Price Transparency

Yes

Yes

No

Dividends

Yes

Yes

Yes

Management Fees

Yes

No

Yes

Benefits

Costs/ Risk

ETF vs Mutual Fund

Transparency

Lower Fees and Transaction Cost

ETF vs Stocks

Diversification

Management Fees

Accessibility

Tracking Error Risk

HOW TO INVEST IN ETFs

The common ways to invest into ETFs include through:

– Brokerages

– Online trading platforms

– Roboadvisors.

If you are interested in adding ETFs into your portfolio, start your account with us at Standard Chartered’s Smart Online Trading Platform.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.