This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

The article is an educational piece about the comparison between dollar-cost averaging and buy-the-dip strategies. For informational purposes only.

If you have been scrolling through Twitter or Reddit (especially on WallStreetBets – notorious for pumping up stocks like GameStop), then you’d probably heard of the term “buy the dip” or “BTD” for short – a piece of pervasive advice that has been promoted by the raft of social media influencers. There is so much limelight over BTD to the extent that the once popular strategy, “Dollar-cost averaging” or “DCA” for short has been overshadowed. Does BTD really reign superiority over DCA?

Different Variations of BTD

While DCA is a plain and simple concept of investing a fixed dollar amount on a regular basis regardless of the asset price, it is not the case for BTD. Unlike DCA, there is more than one way which an investor can buy the dip. The most adopted BTD approach is based on percentage-drawdown. This means buying after a certain percentage dip such as 10%, 20% or 30%. Another BTD strategy is the use of technical indicators such as the moving-average. To better visualize this approach, figure 1 below shows that the S&P 500 index has been in a strong bullish trend and during all this time, the index has remained above the 100-day moving average. Therefore, when it makes a major pullback, you could buy the dip whenever it hits the 100-day moving average.

Figure 1: S&P 500 Index overlayed with 100-day moving average

To avoid drilling into the granular details and over-complicating matters, this article seeks to focus on BTD approach i.e., percentage-drawdown based. Now, back to the comparison!

Setting up the arena for the comparison

To start, let’s say you were given $100 at the start of every month to invest in the S&P 500 index for the next 15 years from Jan 2007 to Dec 2021 with two investment strategies to choose from:

• Dollar-cost averaging (DCA): You invest $100 at the start of every month for 15 years

• Buy the Dip (BTD) – 10%/20%/30%: You save $100 cash at the start of each month until the market retraces 10% from its previous month-end highs. Then, invest all your saved-up cash. Continue saving $100 each month and invest everything until the next 10% dip occurs. Repeat the process for the 20% and 30% dips BTD strategies

1) For simplicity, intra-month highs and lows are ignored.

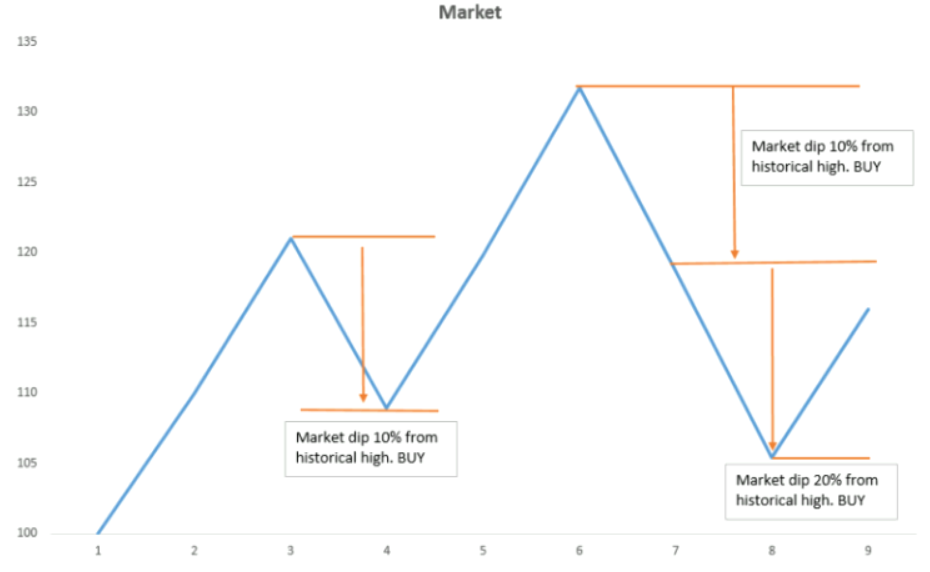

2) To help you understand this better, suppose we start with the 10% BTD strategy. At the start of each month, let’s compare the closing price of the previous month vs the closing price of the prior historical high month during the 15-year period. If the price falls at or more than 10% from the prior historical high, the uninvested cash will be put to work. If the price continues to fall at subsequent 10% dips, the cumulative savings will be invested accordingly.

• Figure 2 below illustrates the hypothetical points of investments using the 10% BTD strategy. Do note that the holding period for every investment was till the end of 2021.

Figure 2: Example of buying the dip at each 10% drawdown

The chart below shows the various entry points of buying the 10% dip (red arrows), buying the 20% dip (yellow arrows) and buying the 30% dip (green arrow). It is evident that as strategies change to allow an increase for a greater magnitude of drawdown/ dip, investors would have less opportunities to buy the dips simply because those drawdowns did not materialize!

Figure 3: Entry levels of buying the dips on S&P 500 Index – buying the 10% dip (red arrows), buying the 20% dip (yellow arrows) and buying the 30% dip (green arrow)

Findings from the comparison: DCA outperformed BTD

The below table showed the findings from the study, it is for illustrative purpose only. DCA yielded the best results in terms of dollar amount profits. However, the amount invested under BTD strategies were noticeably reduced while waiting for the price to drop further. The opportunity costs of staying uninvested were the greatest for the 30% BTD strategy.

DCA

BTD at each 10% drawdown

BTD at each 20% drawdown

BTD at each 30% drawdown

Total Amount invested (a)

$18,000.00

$15,900

$2,300.00

$2,200.00

Market Value of investments after 15 years (b)

$50,172.02

$35,933.64

$9,644.97

$10,823.84

Profits (b) -(a)

$32,72.02

$20,033.64

$7,344.97

$8,623.84

Table: Dollar amount of investments, market value and profits

Parting Words

I am never a fan of a “one-size fits all” belief. Although the above study concluded that DCA was a better strategy than BTD, it is by no means a proclamation that the former is the most superior investment strategy or the most suitable investment approach for all. Results could differ if it was done on a different market and period. But it does highlight the opportunity costs of staying uninvested while waiting for dips. Furthermore, BTD can be time-consuming as it requires additional monitoring. There is also an added complexity should there be more conditions being enacted before the BTD strategy can be executed.

Savvy and/or well-informed investors may still prefer BTD strategy if they have a constructive view of the security after performing their own fundamental or quantitative analysis and research. For example, they may establish a fair value price of a particular security. Thus, they are comfortable to accumulate more on further price weakness.

But for most investors, would it be better to employ DCA? My answer is ‘yes’ if you subscribe to the following main benefits1:

1) Prevent procrastination: Some of us just have a hard time getting started. We know we should be investing, but we never quite get around to doing it. DCA forces you to put your uninvested cash to work consistently.

2) Avoid market timing: DCA ensures that you will participate in the stock market regardless of current conditions. It will eliminate the temptation to try market-timing strategies that are not easy to succeed even for sophisticated clients. As the saying goes, time in the market is more important than timing the market!

About the writer

Kelvin started his career as an Equity Analyst before moving on to advisory roles for both retail and institutional portfolios. With a strong background in technical analysis, Kelvin sees Fibonacci lines, Elliot Waves and chart patterns above his bed, à la Beth Harmon in the Queen’s Gambit. He also enjoys culinary movies, such as “Chef” and “Julie & Julia”, as they delve into the neuroticism of ideas and end in the satisfaction of creating something beautiful, put together with simple, unassuming ingredients, somewhat like working out an investment portfolio. When he’s not obsessing about the financial markets, Kelvin appreciates quality time with friends and family over a game of darts.

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments.

This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you. You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

This document is being distributed for general information only and is subject to the relevant disclaimers available here. It is not and does not constitute research material, independent research, an offer, recommendation or solicitation to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This document is for general evaluation only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person or class of persons and it has not been prepared for any particular person or class of persons. You should not rely on any contents of this document in making any investment decisions. Before making any investment, you should carefully read the relevant offering documents and seek independent legal, tax and regulatory advice. In particular, we recommend you to seek advice regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs, before you make a commitment to purchase the investment product. Opinions, projections and estimates are solely those of SCB at the date of this document and subject to change without notice. Past performance is not indicative of future results and no representation or warranty is made regarding future performance. Any forecast contained herein as to likely future movements in rates or prices or likely future events or occurrences constitutes an opinion only and is not indicative of actual future movements in rates or prices or actual future events or occurrences (as the case may be). This document must not be forwarded or otherwise made available to any other person without the express written consent of the Standard Chartered Group (as defined below). Standard Chartered Bank is incorporated in England with limited liability by Royal Charter 1853 Reference Number ZC18. The Principal Office of the Company is situated in England at 1 Basinghall Avenue, London, EC2V 5DD. Standard Chartered Bank is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. Standard Chartered PLC, the ultimate parent company of Standard Chartered Bank, together with its subsidiaries and affiliates (including each branch or representative office), form the Standard Chartered Group. Standard Chartered Private Bank is the private banking division of Standard Chartered. Private banking activities may be carried out internationally by different legal entities and affiliates within the Standard Chartered Group (each an “SC Group Entity”) according to local regulatory requirements. Not all products and services are provided by all branches, subsidiaries and affiliates within the Standard Chartered Group.

Market Abuse Regulation (MAR) Disclaimer Banking activities may be carried out internationally by different branches, subsidiaries and affiliates within the Standard Chartered Group according to local regulatory requirements. Opinions may contain outright “buy”, “sell”, “hold” or other opinions. The time horizon of this opinion is dependent on prevailing market conditions and there is no planned frequency for updates to the opinion. This opinion is not independent of Standard Chartered Group’s trading strategies or positions. Standard Chartered Group and/or its affiliates or its respective officers, directors, employee benefit programmes or employees, including persons involved in the preparation or issuance of this document may at any time, to the extent permitted by applicable law and/or regulation, be long or short any securities or financial instruments referred to in this document or have material interest in any such securities or related investments. Therefore, it is possible, and you should assume, that Standard Chartered Group has a material interest in one or more of the financial instruments mentioned herein. Please refer to https:// www .sc. com/en/banking-services/market-disclaimer.html for more detailed disclosures, including past opinions/ recommendations in the last 12 months and conflict of interests, as well as disclaimers. A covering strategist may have a financial interest in the debt or equity securities of this company/issuer. This document must not be forwarded or otherwise made available to any other person without the express written consent of Standard Chartered Group.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.