This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

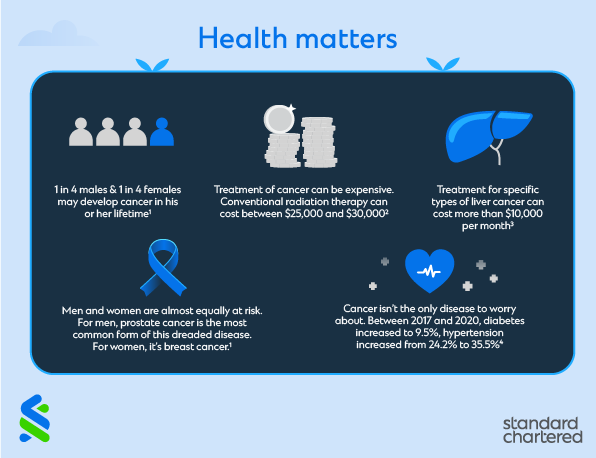

Many of us get so busy with our daily lives we don’t take time to consider about the importance of protection from unexpected adverse situations.

Yet, life throws unexpected situations at us all the time. Some we like, for example winning a lucky draw prize, and others we don’t. Our household income and expenses may be impacted by an illness of someone in the family, or in a more serious situation, the death of the breadwinner of a family. Outstanding loans still need to be repaid, and large sums of money may be required for our children’s education.

While we cannot prevent such situations, we can opt to give ourselves a bit of protection. Protection is not all that complicated once you get down to it.

Here’s a quick look at the precautions you can take to protect yourself and your loved ones, as well as any gaps you may need to take note of.

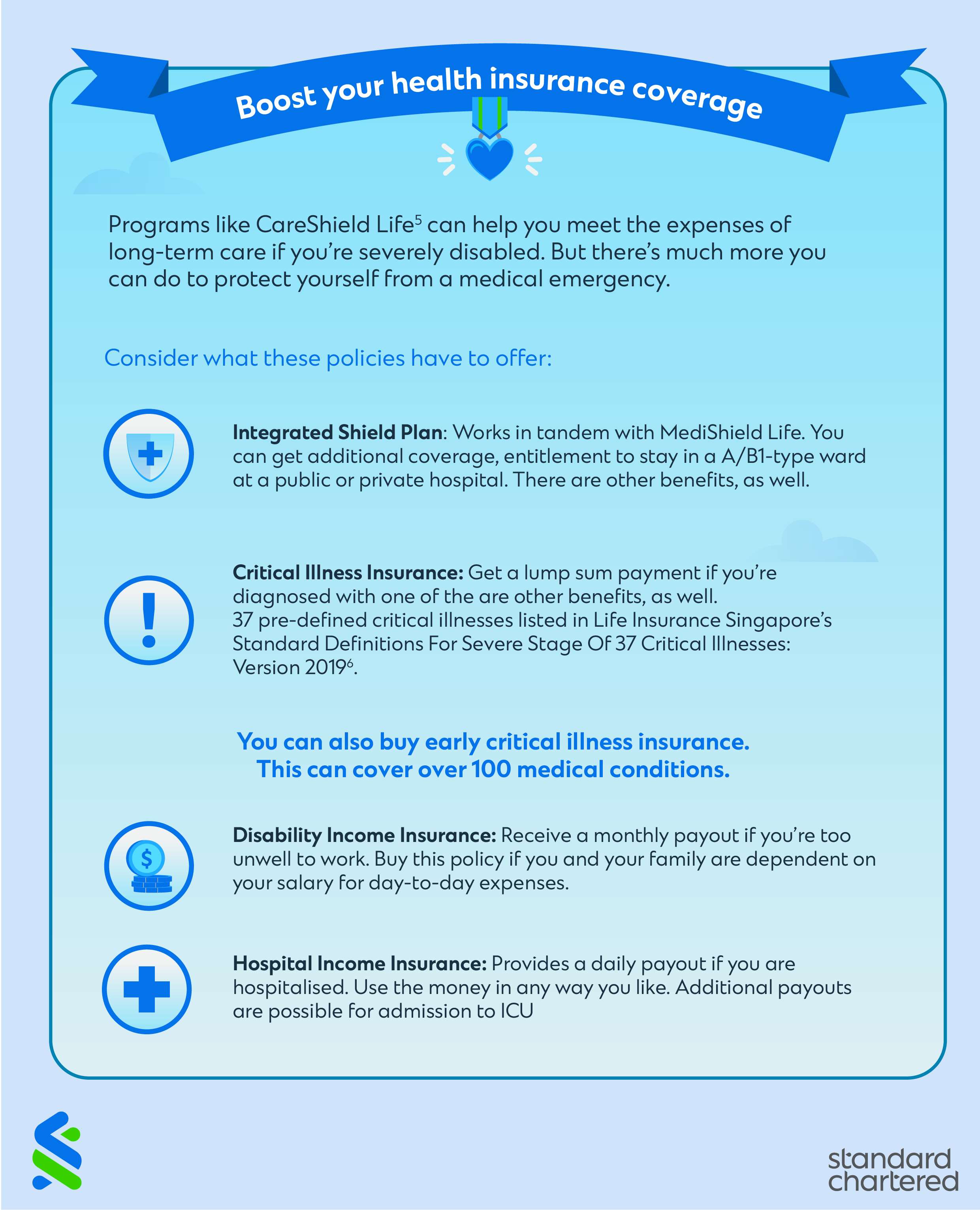

Boost your health insurance coverage

Programs like Careshield Life5 can help you meet the expenses of long-term care if you are severely disabled. But there is much more you can do to protect yourself from a medical emergency. Consider what these policies have to offer: Integrated Shield Plan, Critical Illness Insurance, Disability Income Insurance, Hospital Income Insurance

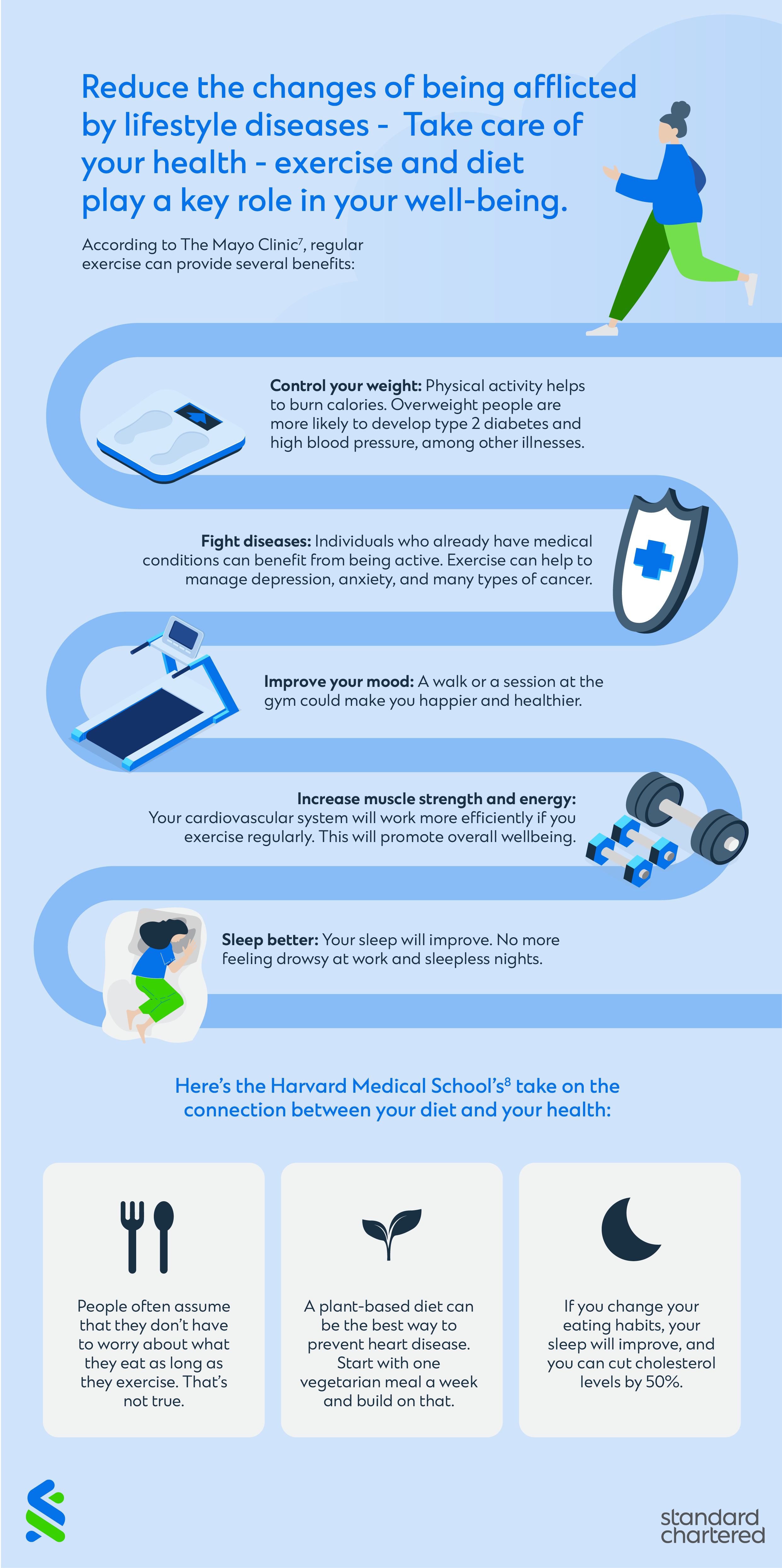

Reduce the chances of being afflicted by lifestyle diseases by taking care of your health. Exercise and diet play a key role in your well-being.

A life insurance policy can provide a solution if the bread winner dies suddenly, and the family faces a cash shortage. So which should you choose – term life or whole life?

Term Life Insurance

Select term life insurance if your primary objective is to provide your family with a lump sum if you pass away.

Term life is economical. Additionally the earlier you buy a policy, the more you save in insurance premiums.

Term insurance provides protection for a specific term. Say, 20 or 30 years.

If you die within the period, your family will get a payout. If you survive, the payout is zilch. You don’t get any money at all.

Term life insurance is not a good option if you can’t bear the thought of paying insurance premiums and getting nothing in return.

Whole Life Insurance

Whole life insurance, as its name implies, covers you for your entire life. So there’s a guaranteed payment at the end.

There could be an additional amount in the form of a bonus, as well.

Whole life insurance is comparatively expensive.

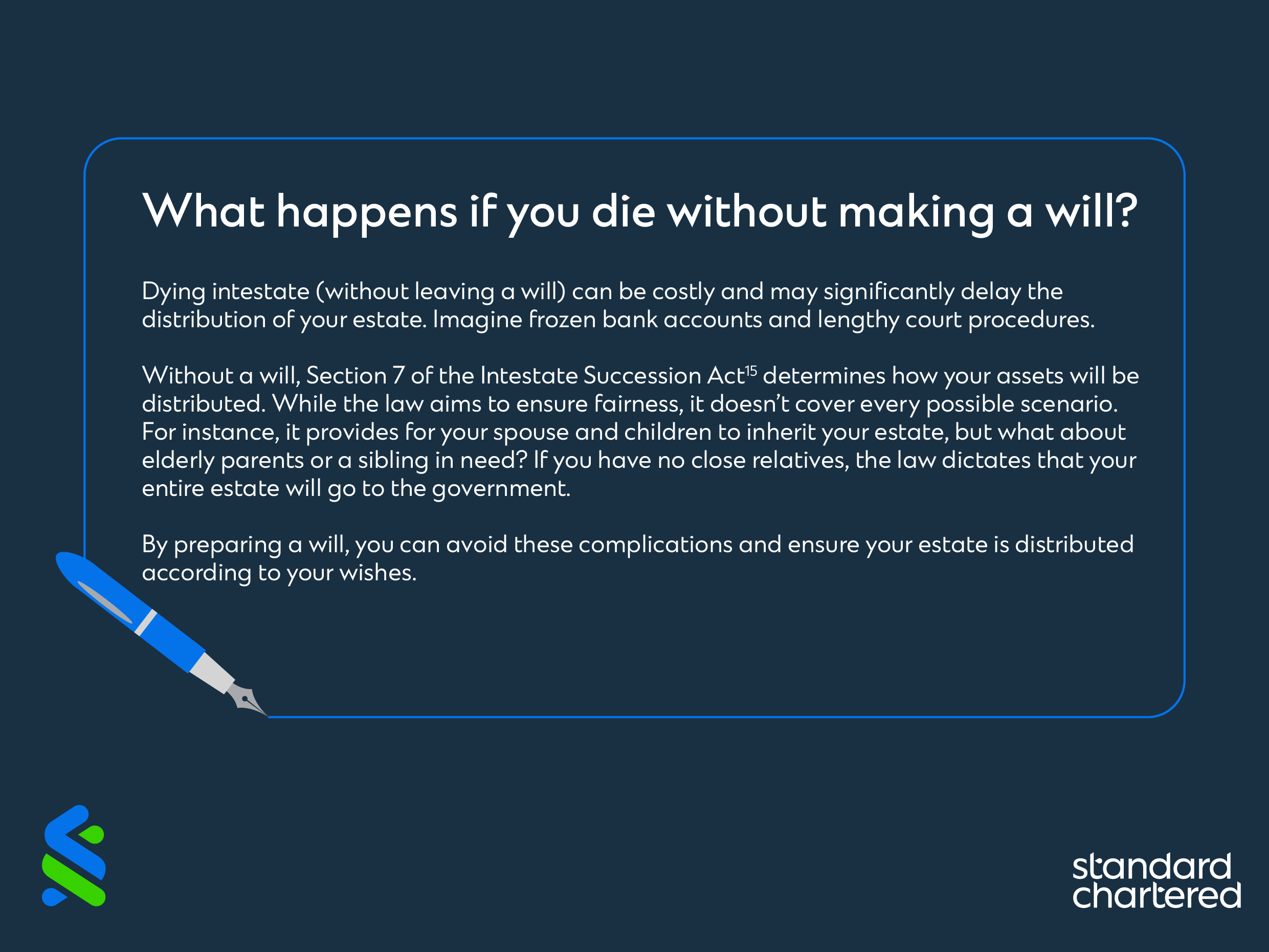

Making a will

A will is a written document that sets out who is going to inherit your estate. That includes your: Property; Cash and other valuables; Other Assets.

A will can assume great significance if there is a disabled or elderly relative whom you are responsible for.

Perhaps the most significant benefit of making a will is that it removes uncertainty among your relatives.

Do all you can to protect your home, which is probably your most valuable asset

If you have HDB fire insurance, you need to buy a separate policy for the contents of your flat. Remember to insure any expensive renovations that you have carried out.

Consider other types of add-ons:

Personal liability cover

Alternative accommodation cover

Often Travelling? Invest in an annual travel insurance plan.

Start future-proofing and protect yourself and your loved ones.

As a first step, you could review your health and life insurance policies. Is your Integrated Shield Plan adequate for your needs? You may want to add more life insurance coverage if your income has gone up. Next, evaluate your home insurance and mortgage insurance. Check if you need to make any changes.

Finally, make your will. This is important if you have children or other dependent family members.

This article is brought to you by Standard Chartered Bank (Singapore) Limited. All information provided is for informational purposes only.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.