This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Insurance is a protective shield that offers you financial security when you most need it. As a thriving millennial, you are not too young to buy insurance and secure your income and future. In fact, investing in insurance at the start of your career will help secure your income at a lower cost.

Finding the optimal insurance mix depends, in large part, on your personal circumstances. Check out this infographic to choose the insurance that is right for your needs.

What are the types of insurance?

Whole Life Insurance: Builds long term cash value that can be withdrawn as annuity pay-outs for your retirement needs

Term Life:Highest coverage at lowest premium; pay-out only in the event of untimely death

Health Insurance:Covers unforeseen health or accident-related eventualities that can significantly impact income

Endowment: Builds cash value that will be paid at the end of a fixed period so you can save for medium-term expenses like children’s higher education

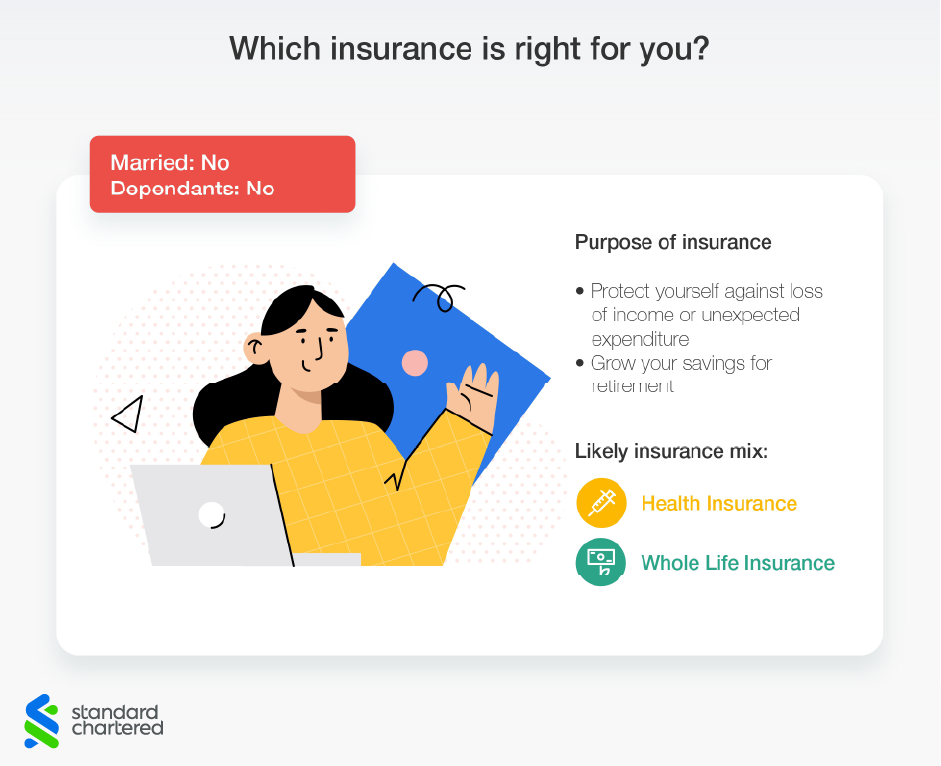

Which insurance is right for you?

Profile: Not Married and have no dependents

Likely insurance mix: Health Insurance, Whole Life Insurance

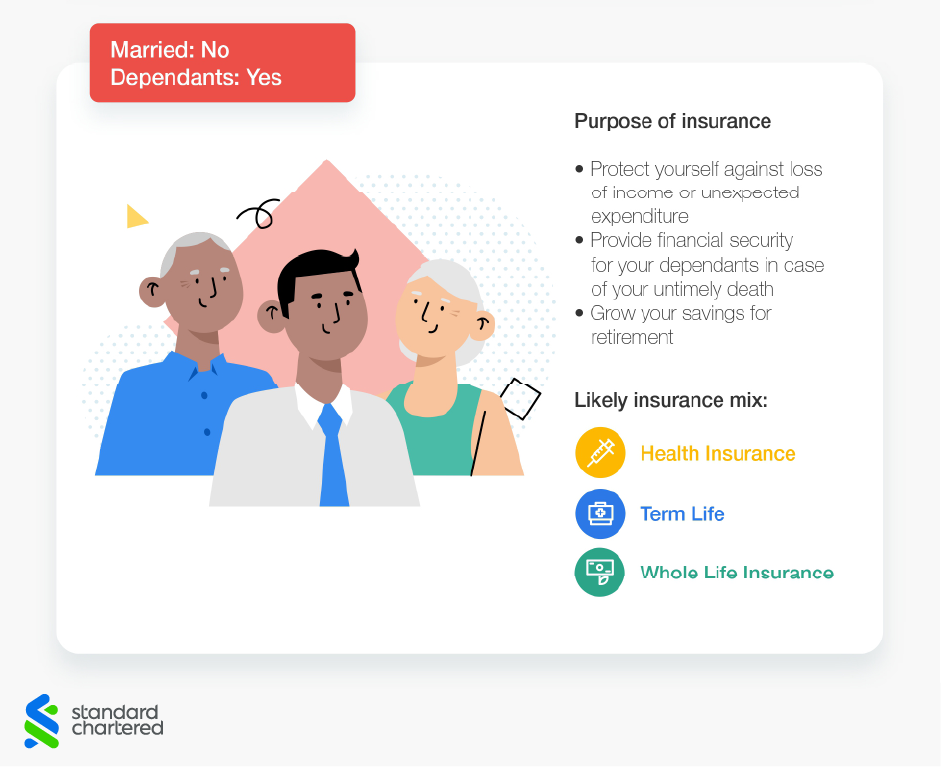

Profile: Not Married and have dependents

Likely insurance mix: Health Insurance, Term Life, Whole Life Insurance

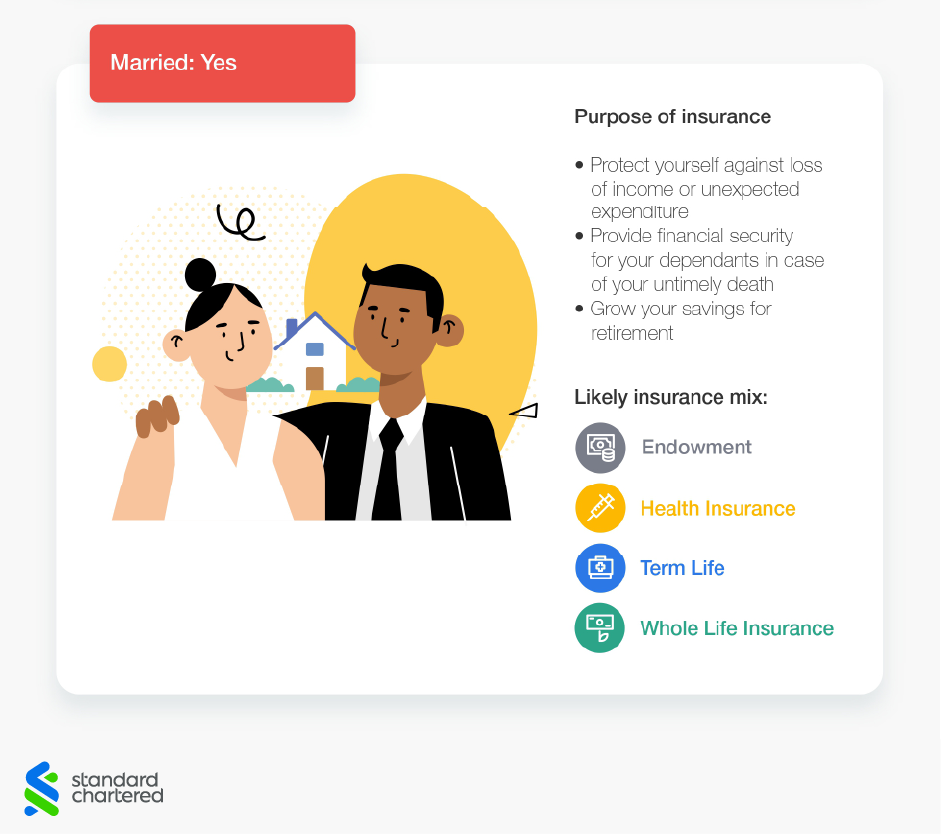

Profile: Married

Likely insurance mix: Endowment, Health Insurance, Term Life, Whole Life Insurance

Your insurance needs will change as you journey through different life stages. Constantly reviewing your long-term needs and mapping them to the relevant insurance products will enable you to smartly secure your future.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication