This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Wealth BuildingForex, Gold & Alternative InvestmentsInvestment Strategies

21 March 2025 I 6 mins read

The US Dollar is expensive by some measures. Staying invested in a globally diversified portfolio is a good way to hedge against any Dollar volatility.

Will the US Dollar remain as the world’s dominant and, by some measures, the most expensive currency? In an increasingly charged geopolitical world, this question has become more and more part of the financial market discussion following several years of sizeable US Dollar strength. Speculation about a possible ‘Plaza Accord’-style agreement to weaken the Dollar has added fuel to the fire. Should investors worry?

The Dollar’s dominance vs. the Dollar’s value

We believe one way to answer these questions is to separate the structural dominance of the US Dollar from the question about valuation, which is a more cyclical question.

The US Dollar continues to be the most dominant currency from both a trade and store-of-reserve perspective. While the Dollar’s share has admittedly reduced in recent decades on both fronts, data from the Bank for International Settlements (BIS) shows the greenback’s share in payment for global trade remains significant, as does its share as a global central bank currency reserve. To an extent, this is not surprising. We have written before about how few other currencies offer the breadth and depth of investment opportunities as the US Dollar. Investors are attracted to the Dollar to make riskier investments targeting higher returns (such as in equities and high yielding bonds) or park their money in relatively stable, high-quality assets (such as government bonds) to preserve capital. Together with the free movement of capital offered by the US, these factors make the Dollar the dominant currency in payments for trade and as a vehicle to hold reserves. We believe this dominance is unlikely to end soon.

This does not mean, however, that the US Dollar’s value will not go through cycles. This is where more significant movement over a multi-year horizon looks more plausible.

The context – what do US Dollar valuations tell us?

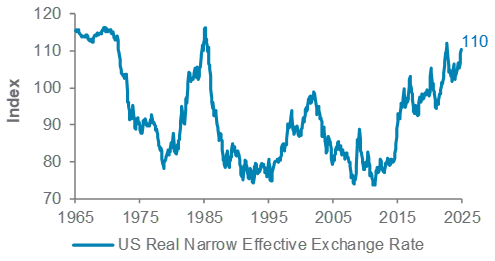

Source: Bloomberg, BIS

The chart above from the Bank for International Settlements illustrates one approach to US Dollar valuations. It shows that the US Dollar is now increasingly expensive on this measure – almost as expensive as during its 1985 peak and significantly more expensive than its 2002 peak. Currency valuations, by themselves, can tell us little about the 12-month outlook. On a multi-year horizon, though, it does suggest the US Dollar is more likely to moderate than continue moving towards ever higher valuations. Similar moderations in value were observed in the second half of the 1980s and the 2000s.

A softer Dollar is likely to help President Trump’s efforts to cut the US’ large trade deficit. In theory, a more moderately valued US Dollar would help rebalance the country’s trade balance by making imports more expensive and exports more competitive. The internationally orchestrated devaluation of the Dollar through the 1985 Plaza Accords followed a similar train of thought. Of course, at that time, the US mainly negotiated with a geopolitical ally, Japan to boost the value of the Yen against the Dollar. It is also plausible to argue that a shift in relative interest rate outlooks could lead to US Dollar moderation. This would typically play out via lower net-of-inflation yields in the US and higher yields elsewhere.

Does this all matter for investors?

Against this backdrop, many investors feel the need to ‘do something’. However, some context may help ensure any action (or lack thereof) is deliberate.

The most important takeaway for investment portfolios is that the ultimate currency exposure of your investment matters. For example, investing in the S&P500 index of US stocks means that you are already significantly exposed to non-US markets, given that about 40% of the underlying revenue exposure of the index companies is sourced from outside the US. This creates a natural hedge. Similarly, many bonds may be denominated in US Dollars, but the underlying income could depend on non-USD sources (such as Emerging Market bonds). Getting, and staying, invested in a diversified portfolio can often be one of the best mitigants against unexpected currency market volatility. This is something we can act on today.

One asset class which tends to have a more direct relationship with the US Dollar is Emerging Markets (EM). EM assets (equities, but also bonds and cash) have historically tended to do well when the US Dollar weakens, and vice versa. Today, we favour a greater tilt towards US assets, given relatively strong US economic and earnings growth and trade and geopolitical uncertainty clouding the outlook of the rest of the world. However, in a scenario where the US Dollar weakens on a multi-year basis, EM assets are likely to do well. That said, we are not there yet.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.