This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

When you take out a house mortgage, purchase an MRTA policy to protect your family home in case of disability or death

Ask an expert: Why you need MRTA insurance for your family home

When you take out a mortgage to purchase a home, some lenders may require that you buy a Mortgage Reducing Term Assurance (MRTA) policy. An MRTA policy takes care of your mortgage payments in the event of your death or, in some cases, a terminal illness or disability. That means your family will be protected from losing their home should a tragedy occur.

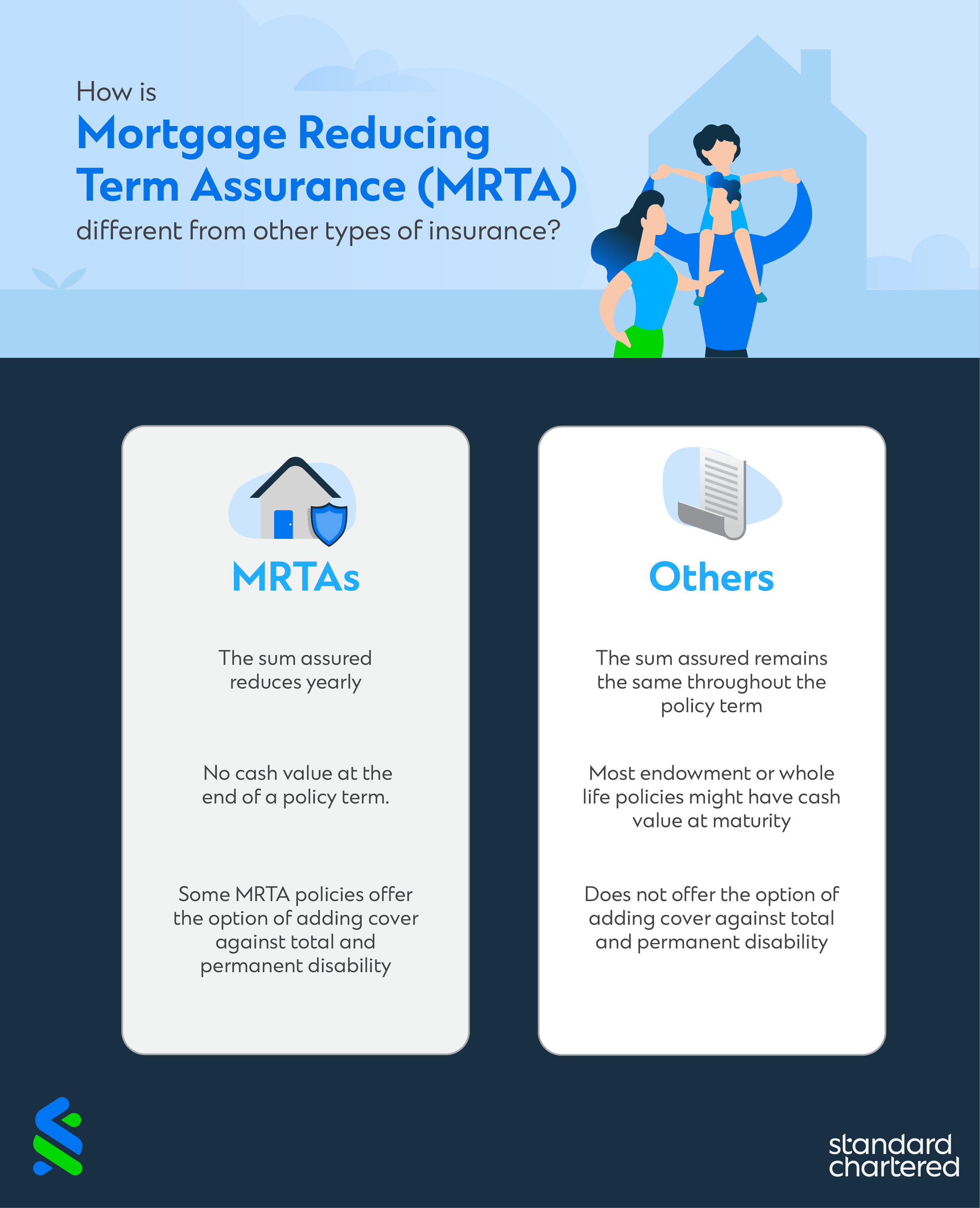

What is MRTA and how is it different from other types of insurance?

MRTA insurance covers the policyholder during the term of the policy by paying off any outstanding mortgage payments that the policyholder’s spouse may be left with. Some MRTA policies also offer the option of adding cover against total and permanent disability until the policyholder turns 70.

The key difference between MRTA and other types of insurance policies relates to the sum assured. Most insurance policies typically set a pre-determined sum assured at the start of the policy term and that remains the same throughout the term of the policy.

In the case of an MRTA, the sum assured can be set at an amount up to the mortgage loan amount at the time the policy is purchased. However, MRTAs are decreasing term policies, which means the sum assured reduces yearly. The rate at which it reduces usually depends on the mortgage interest rate that is determined at the onset of the policy.

This generally means that there is no cash value at the end of a policy term, as opposed to most other endowment or whole life policies that might have cash value at maturity.

What are the benefits of MRTA?

The obvious benefit is that MRTA protects your family from losing their home. But there are additional benefits that different plans offer — think of these as benefits that make a particular plan more attractive.

For example, PRUmortgage offers flexible terms of 10 to 35 years with a choice of interest rates that range from one to seven per cent. Also, you may not have to undergo a medical examination if the policy is taken up within three months from the mortgage loan and for a sum assured of under S$1 million.

Also, an Accelerated Terminal Illness or Disability Benefit Advance may be paid out if the policyholder becomes totally or permanently disabled, or is diagnosed with a terminal illness. Once this amount is paid out, the sum assured for death will usually be reduced accordingly.

PRUmortgage also offers joint-life (for a couple) or single-life policies. There may be a premium discount available if you purchase as a joint-life policy.

Are there any Singapore-specific exclusions or other considerations that I should be mindful about?

There may be some standard exclusions depending on the terms of your particular MRTA policy. These exclusions may include things like a pre-existing terminal illness, self-inflicted injuries, AIDS, AIDS-related complex, pregnancy or any related complication, participating in hazardous activities, any aerial activity, competitive or professional sports, and the improper use of alcohol. Any exclusions that apply to you specific MRTA should be listed in your policy document. Read it carefully and make sure you understand any and all exclusions.

Taking out a mortgage protection policy will offer you the peace of mind of knowing that in case of a terminal illness or death, your loved ones won’t lose the family home.

Your feedback is valuable to us. Did you find this article helpful?

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount.

Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication