Diversify your portfolio with Debt Securities Services like Bonds and Structured Notes

-

Not having Debt Securities Account?

Not having Debt Securities Account?

Need more information?

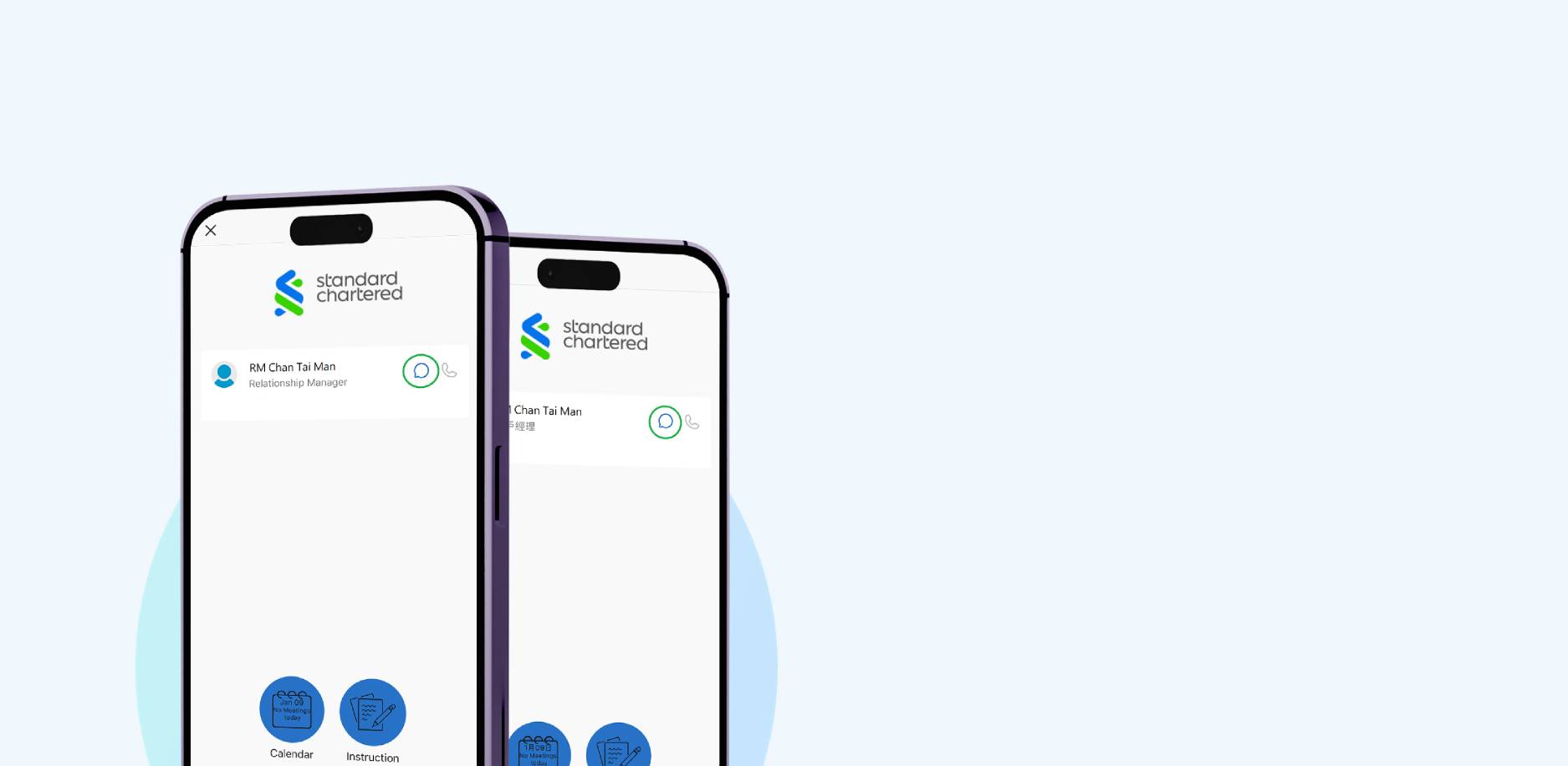

Consult our RM to learn more on Debt Securities

Via SC Mobile App

Use mobile device (iOS App or Android App) to click the following button. Simply click “myRM” button

Via Online Banking

Login Online Banking and select “myRM” from the menu