One of the biggest investment debates of our times is whether to own cash or government bonds. In the Developed Markets, one of the most rapid policy rate hiking cycles in history has meant that short-term returns from cash are now higher than what one can earn on a longer maturity bond. Unsurprisingly, this has led to a significant move into cash deposits or money market funds across major economies around the world.

Despite this, many asset allocators (ourselves included) continue to advocate the case for high quality bonds over cash. Are the yield optics sending investors a false signal?

If yields were the only drivers of total investment returns, then there would be little debate on which asset to choose – one could simply allocate to the asset class with the highest yield. In today’s market, that would be cash.

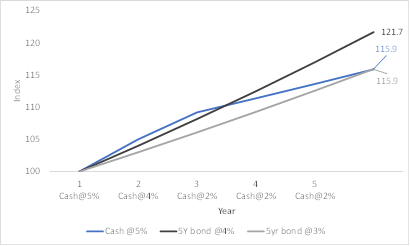

However, one needs to dig a little deeper in the investment world to figure out the real value of the two competing assets. The trade-off is best illustrated with a simple example. In the chart below, we compare three scenarios over a 5-year horizon:

The chart illustrates how an investor’s returns pan out over the five-year period. In the first year, cash is clearly ahead with its higher yield.

However, as the one-year cash yield starts to drop in later years, returns fall rapidly. When the investor looks back with hindsight after 5 years, the 5-year bond yielding 4% (1 full percent below the cash yield) ended up being the investment that delivered the highest returns.

Cash only ended up matching returns for a 5-year bond that yielded 3%.

Leaving aside the need for liquidity, some cash can make sense within an investment allocation. This was not really the case for a large part of the previous cycle when cash yields largely went to zero. However, ever since central banks began to raise rates rapidly, cash has become a little more competitive.

Nevertheless, there is little reason to expect cash to do a better job of preserving wealth in real (or inflation-adjusted) terms compared with riskier asset classes. The Optical yield illusion is making many investors respond to the headline yield on cash, but high-quality bonds are the hidden gems that are likely to outperform cash and better keep up with inflation over the coming years.